The Invisible Front: US-Iran War's Food Shock

The US-Iran war shut the Strait of Hormuz. The world noticed the oil price. Nobody noticed that a third of global fertilizer trade just stopped moving — right before planting season. The harvest damage is already locked in. The hunger is still coming.

The Unseen War

A young minister once approached an old monk in a drought-stricken land.

“Master,” he said, “the war is far away. The bombs fall across seas. Why then are our fields failing, our markets tightening, and our people anxious?”

The monk picked up a handful of dry soil and let it fall through his fingers.

“Tell me,” he asked, “what feeds the grain?”

“The rain,” said the minister.

“And before the rain?”

“The seeds.”

“And before the seeds?”

The minister paused.

“The unseen,” the monk said gently. “The soil’s strength. The nutrients beneath the surface. The quiet work no one praises.”

The minister frowned. “But what has that to do with war?”

The monk pointed to a distant caravan road.

“When the road is cut, the carts stop. When the carts stop, the soil starves. When the soil starves, the grain weakens. And when the grain weakens, the people suffer.”

“But the war is not here,” the minister insisted.

The monk smiled. “You see distance. The earth sees a connection.”

He continued, “A famine does not arrive with drums. It begins in silence — in ships that do not sail, in factories that do not produce, in choices farmers make when they have less than they need.”

The minister looked again at the dry soil.

“So the crisis began long before we felt it?”

The monk nodded.

“And it will continue even after peace is declared?”

The monk closed his eyes.

“The field remembers what the world forgets. By the time hunger speaks, the causes are already past.”

The wind carried the dust away.

And for the first time, the minister understood that the deepest wars are the ones no one sees.

The War Behind the War

When the United States and Israel launched coordinated strikes on Iran on February 28, 2026, under what Pentagon planners called Operation Epic Fury, the world's attention snapped to the obvious: oil prices, the Strait of Hormuz, the risk of regional escalation.

These are the crises that command television coverage and emergency G7 calls.

But a quieter catastrophe was already unfolding in the background, one measured not in barrels of crude but in metric tons of urea, ammonia, and phosphate — the invisible architecture that underpins the food security of more than eight billion people.

About one-third of global seaborne trade in fertilizers typically passes through the Strait of Hormuz, which has been nearly entirely closed since the United States and Israel attacked Iran on February 28. That single statistic, buried beneath breathless coverage of drone strikes and oil futures, is arguably the most consequential fact of the entire conflict.

Because, unlike oil, which nations stockpile strategically and for which alternatives can sometimes be found, fertilizer operates on an unforgiving biological calendar.

The crisis has three distinct layers that are analytically inseparable. The first is the direct disruption to fertilizer exports from the Gulf. The second is a less-discussed upstream problem: the disruption to the natural gas feedstock that the rest of the world needs to manufacture fertilizer domestically. The third, and potentially most catastrophic, is the time-locked nature of the crisis — the fact that even a ceasefire signed today would leave the global food system dangerously short for this growing season, because even if the Strait of Hormuz does open soon, restarting production and transport for fertilizers and their components could take weeks — weeks that Northern Hemisphere farmers do not have.

With this, let us attempt a full 360-degree analysis of this slow-motion famine machine — tracing its mechanics through every major producing and consuming nation, examining its human cost across Asia and Africa, and testing the extraordinary hypothesis that the GCC states themselves, the very exporters of fertilizer whose strategic location is at the center of this crisis, face an existential food and water emergency that could render them ungovernable.

The Fertilizer Architecture: How the Gulf Became the World's Nutrient Hub

To understand the crisis, you must first grasp how thoroughly the global fertilizer system became concentrated in a single geopolitically volatile region.

Nitrogen dominates global fertilizer use, accounting for roughly 59% of total consumption in 2023, far ahead of phosphorus (21%) and potassium (20%).

Its importance is not accidental—nitrogen is fundamental to plant growth, driving protein formation and enhancing photosynthesis, which directly impacts crop yields. Nearly 45% of nitrogen-based fertilizers are used to cultivate staple crops such as wheat, rice, and maize (Source: IMARC) —foods that together supply over 40% of the world’s caloric intake.

Over human history, out of about 30 000 edible plant species, 6 000 – 7 000 species have been cultivated for food. Yet, today we only grow approximately 170 crops on a commercially significant scale. Even more surprising, we depend highly on only about 30 of them to provide us with calories and nutrients that we need every day. More than 40 percent of our daily calories come from three staple crops: rice, wheat and maize! (Source: Nearly half our calories come from just 3 crops. This needs to change / World Economic Forum)

In simple terms, modern food security is tightly coupled with steady access to nitrogen.

This creates a structural vulnerability. Grain producers depend heavily on stable nitrogen fertilizer supplies, yet production and inputs are geographically concentrated. The Middle East plays a pivotal role, both as a major exporter of liquefied natural gas (a key input for synthetic nitrogen fertilizers) and as a supplier of fertilizers like urea and ammonia. Much of this trade flows through the Strait of Hormuz, a narrow but critical chokepoint.

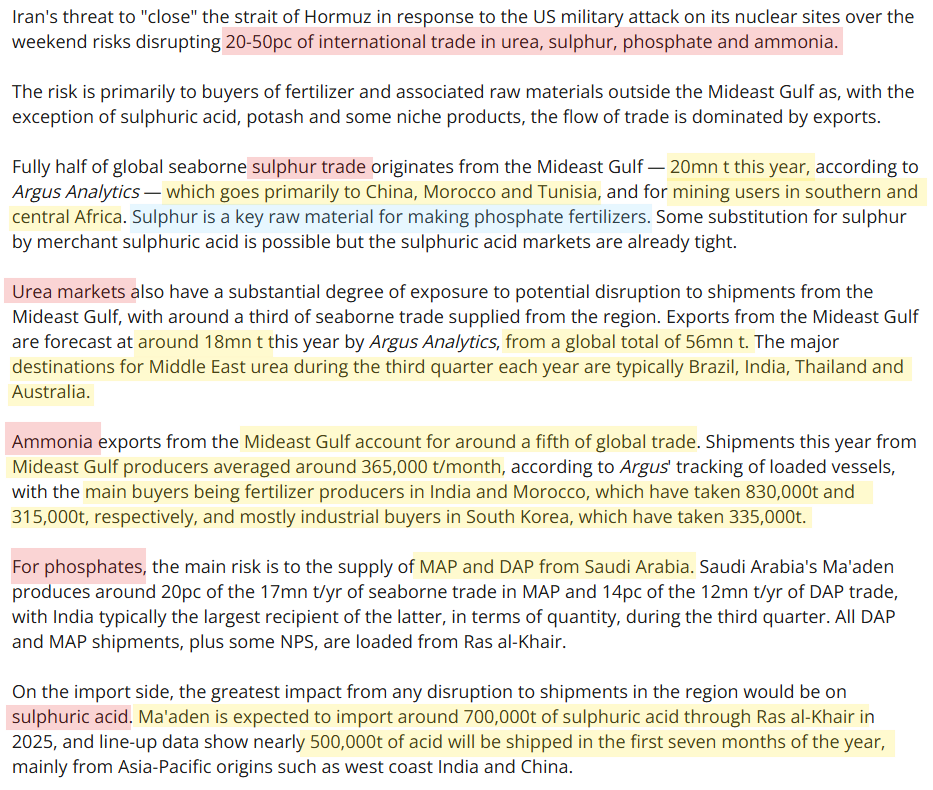

The Strait alone handles about 20% of global LNG exports and between 20–30% of global fertilizer trade, including roughly 35% of urea exports.

The phosphate picture compounds the vulnerability. The phosphate fertilizer trade carries its own risks. Approximately 20 percent of global phosphate fertilizer trade originates from countries affected by the strait's disruptions or the broader regional conflict, with Saudi Arabia and Israel together accounting for 17 percent of global phosphate fertilizer exports. Furthermore, sulfur, a byproduct of oil and gas processing, is also critical for phosphate fertilizer production. Approximately 45 percent of the global sulfur trade is affected by disruptions caused by the conflict.

Sulfur — the largely overlooked third element — is what converts phosphate rock into a form that plant roots can actually absorb. Without Gulf sulfur, phosphate fertilizer plants from Morocco to China operate below capacity. The disruption is therefore not merely of finished fertilizer flows but of the entire upstream industrial chemistry that makes modern agriculture possible.

Sarah Marlow, global head of fertilizer pricing at Argus, noted that the unfolding crisis would have a bigger impact on the fertilizer trade than the Russia-Ukraine war.

"Almost 50% of all globally traded sulfur comes from that region. For urea, it's around a third of all globally traded urea that comes from that region and for ammonia, it's close to 25%." (Source: It’s not just oil and gas. The Strait of Hormuz blockage is rattling another vital commodity / CNBC)

She emphasized that unlike Ukraine, multiple producers are now being affected simultaneously — Saudi Arabia, Kuwait, Qatar, Iran and the United Arab Emirates all disrupted at once.

Any disruption in this corridor can ripple quickly into global food systems, amplifying price shocks and threatening agricultural output worldwide. And that is precisely what the world is witnessing right now.

This is the key analytical difference between this crisis and 2022.

The Cascade: From the Strait to the Farm

The crisis does not operate in a single direction. It is better understood as a cascade — each disruption triggering the next, each price spike feeding the one downstream.

It's not just that Gulf fertilizer can't reach export markets such as Sudan, Brazil, or Sri Lanka.

It's also that fertilizer producers elsewhere lack key ingredients — the second-order effects of a supply chain crisis. (Source: The Other Global Crisis Stemming From the Strait of Hormuz’s Blockage / Carnegie Endowment).

This point deserves unpacking.

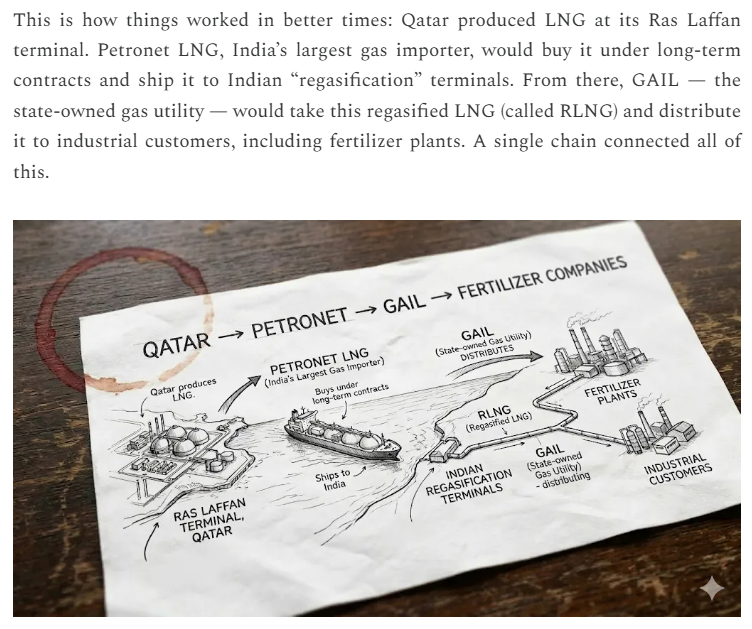

India manufactures roughly 28–29 million tons of urea domestically, against annual consumption of 35–36 million tons. The difference is imported, mostly from the Gulf. But Indian domestic production itself relies on LNG imports from Qatar to fuel its plants.

On 3 March 2026, Petronet told stock exchanges that its LNG vessels could no longer safely transit Hormuz to reach Ras Laffan. It invoked force majeure. Suddenly, GAIL couldn't get LNG from Petronet, hitting fertilizer plants almost immediately. GNFC — Gujarat Narmada Valley Fertilizers & Chemicals — disclosed that its allocation from GAIL was cut to 60% of its daily contracted quantity, starting 6 March.

India’s response offers a clear view into how states manage scarcity under pressure. Decisive, but revealing of underlying vulnerabilities.

The Natural Gas Supply Regulation Order, 2026, issued under the Essential Commodities Act, formalizes a strict hierarchy for allocating limited gas supplies.

At the top of this order are households: piped natural gas for cooking, compressed natural gas (CNG) for transport, and LPG production are fully protected, receiving 100% of their required allocation. This reflects a political and social imperative—shielding everyday consumption to maintain stability.

The real risk lies in timing. If these restrictions persist into the June monsoon sowing season, the consequences could be severe.

Kharif crops (rice, pulses, and other staples) are highly sensitive to fertilizer availability. Reduced application rates could depress yields across large parts of the country, with cascading effects on food prices and rural incomes.

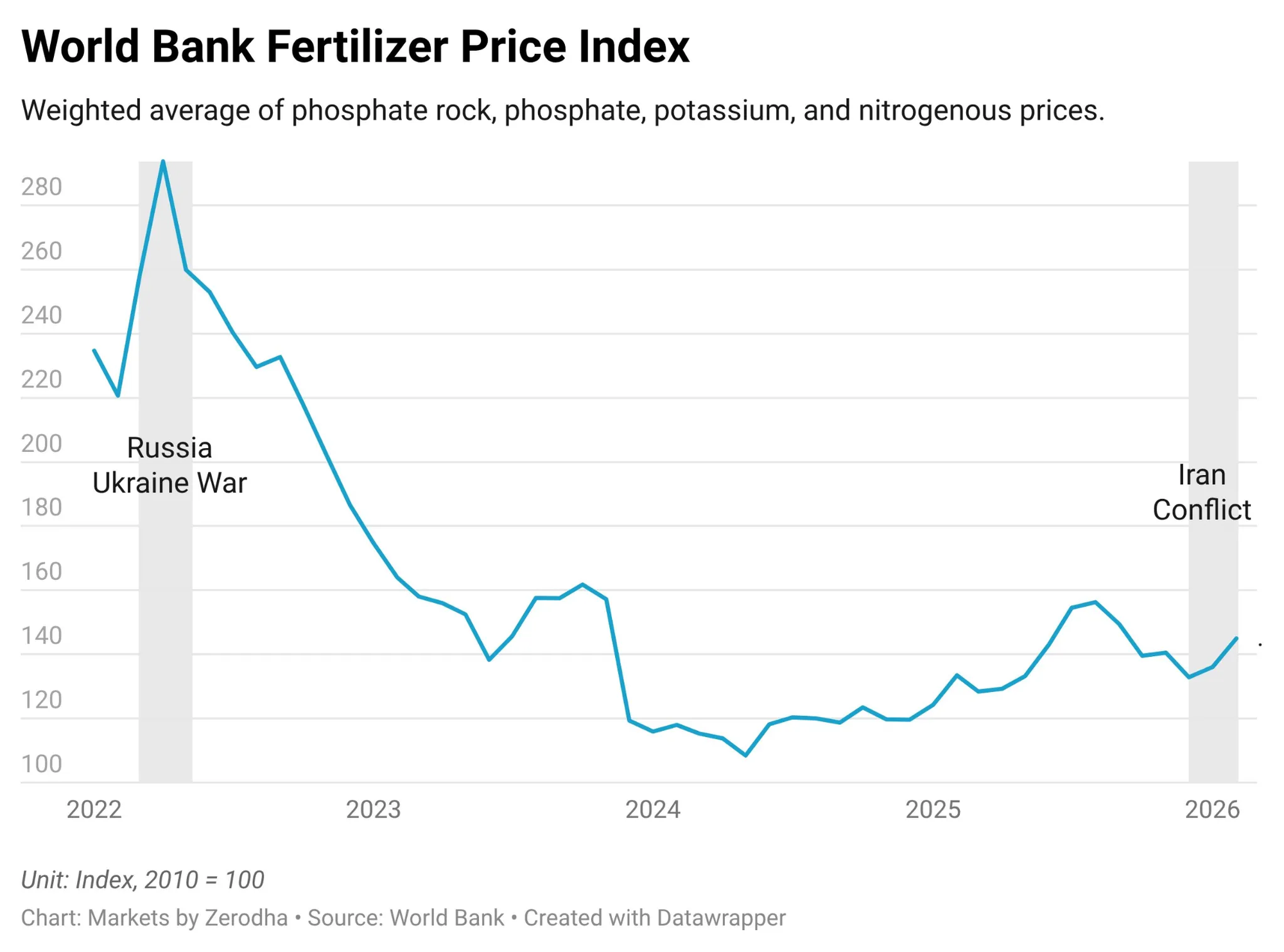

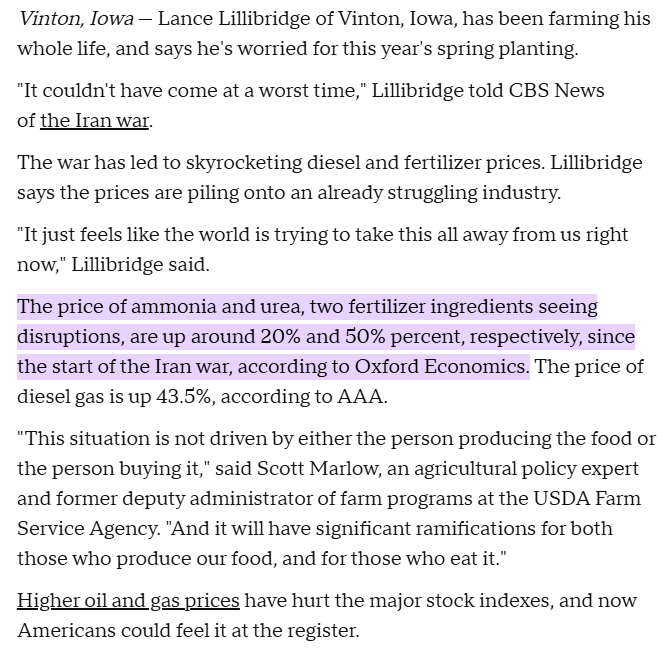

Bangladesh has had to shut down fertilizer factories as Middle East crisis strains gas supply. Egypt has lost its gas imports from Israel and must turn to the ever-pricier LNG market. The benchmark price of urea, the most widely traded fertilizer, is up about 30 percent in the last month.

The price signal is clear and alarming. Analysts working in the fertilizer sector report that the cost of FOB granular urea in Egypt — a bellwether of nitrogen fertilizers — jumped to around $700 per metric ton, up from $400 to $490 before the war began.

Urea and ammonia prices have surged by around 50 percent and 20 percent, respectively, since the war began.

For context, one ton of urea costs U.S. farmers the equivalent of 75 bushels of corn in December 2025; by early March, one ton of urea costs the equivalent of 126 bushels. The affordability ratio for fertilizer versus crop output — what the Rabobank urea affordability index tracks — has fallen to its second-lowest level since 2010. Farmers across the Northern Hemisphere face the same brutal arithmetic: fertilizer costs have risen faster than the value of the food they will produce.

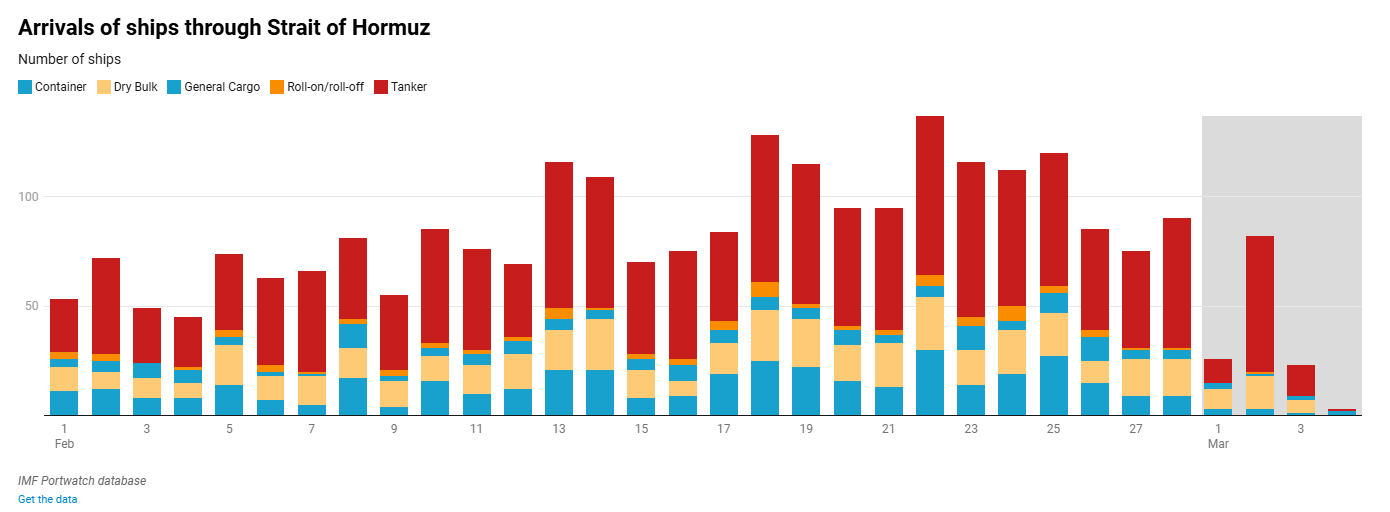

The United States relies heavily on nitrogenous fertilizer imports, with Russia and Qatar as its top suppliers of urea. Urea prices at the New Orleans import hub jumped 32 percent, from $516 per metric ton on Friday, February 27, to $683 on Thursday, March 5. According to one advisory firm, one ton of urea cost U.S. farmers the equivalent of 75 bushels of corn in December 2025, while this week, one ton of urea costs the equivalent of 126 bushels. The firm estimates that urea prices jumped 77 percent from mid-December 2025 to March 9, 2026. The strait’s closure is particularly ill timed for U.S. agricultural producers, as the spring planting season sees the largest volumes of fertilizer imports on average (see Figure 1). Vessels traveling from the Persian Gulf to the U.S. Gulf coast typically take 30 days, meaning supply disruptions today could adversely affect peak spring planting windows in March and April. U.S. fertilizer markets lack strategic reserves and domestic production cannot scale quickly enough to offset sudden import disruptions, especially during spring planting seasons. (Source: Chokepoint: How the War with Iran Threatens Global Food Security / CSIS)

The rational farmer's response is to apply less fertilizer or switch to less input-intensive crops. Either outcome reduces yields.

Grain prices today remain below the peaks seen during the Russia-Ukraine War, squeezing farmer margins. In response, farmers may shift to less fertilizer-intensive crops—such as soybeans in the U.S., or reduce fertilizer use altogether. Both choices come at a cost: lower yields.

And lower yields inevitably translate into higher consumer prices.

Fertilizer prices are below the peaks seen after Russia’s invasion of Ukraine, but grain prices were higher then, helping farmers absorb the costs, said Joseph Glauber of the International Food Policy Research Institute. Grain prices are lower now meaning margins are tighter and farmers may have to switch to less fertilizer-intensive crops — such as soybeans in the U.S. — or apply less fertilizer, reducing yields. Lower yields can lead to higher consumer prices. (Source: The war in Iran sparks a global fertilizer shortage and threatens food prices / ABC)

The paradox is stark. Measures taken to protect farmers’ immediate economic interests end up intensifying the broader food crisis. In trying to stay afloat, producers may unintentionally deepen the very instability they are struggling to survive.

The GCC's Existential Paradox: The Fertilizer Exporter That Cannot Eat

Here lies the most analytically underexplored dimension of the entire crisis: the Gulf states are simultaneously the world's fertilizer exporters and its most food-insecure advanced economies.

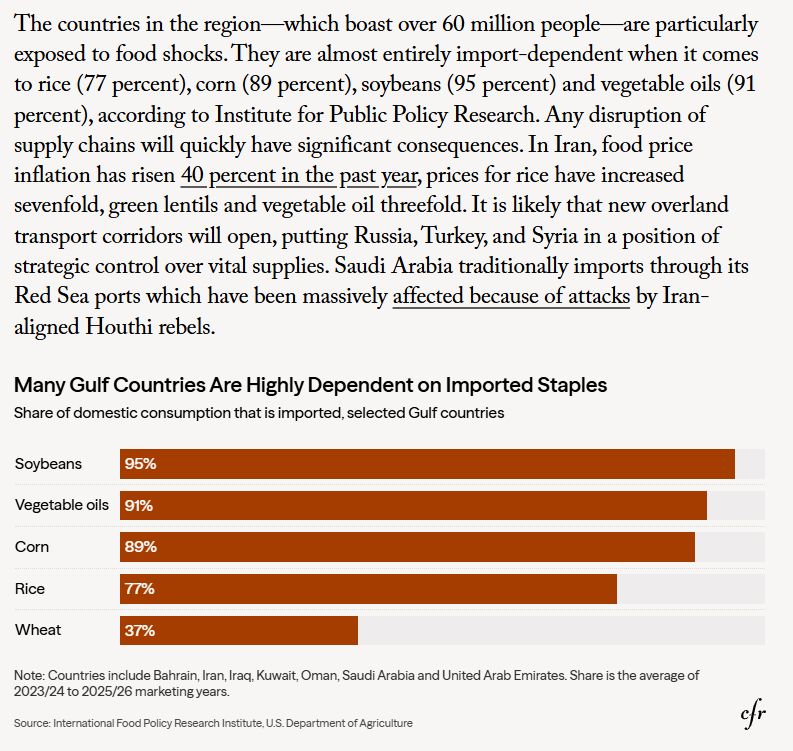

These countries are structurally vulnerable to external shocks because their food systems depend overwhelmingly on imports: 77% for rice, 89% for corn, 95% for soybeans, and 91% for vegetable oils.

This means even minor disruptions—whether from conflict, shipping bottlenecks, export bans, or price spikes—can rapidly translate into domestic shortages and inflation. With over 60 million people affected, the margin for error is thin.

Governments have limited buffers, and supply insecurity can quickly escalate into social unrest. In such systems, food is not just an economic commodity—it becomes a strategic risk, tightly linked to political stability and national security.

These are not the numbers of a developing nation engaged in subsistence farming. These are the numbers of states that chose to monetize hydrocarbons and import everything else — a perfectly rational strategy under conditions of stable global trade. Those conditions no longer exist.

By mid-March, an estimated 70 percent of the GCC region's normal food imports had been disrupted, with retailers airlifting staples and consumer food prices up 40 to 120 percent depending on the product. GCC citizens, accustomed to some of the most heavily subsidized and abundant food environments in the world, are experiencing price shocks without modern historical precedent in their context.

But food insecurity is only one layer. Water is arguably more acute.

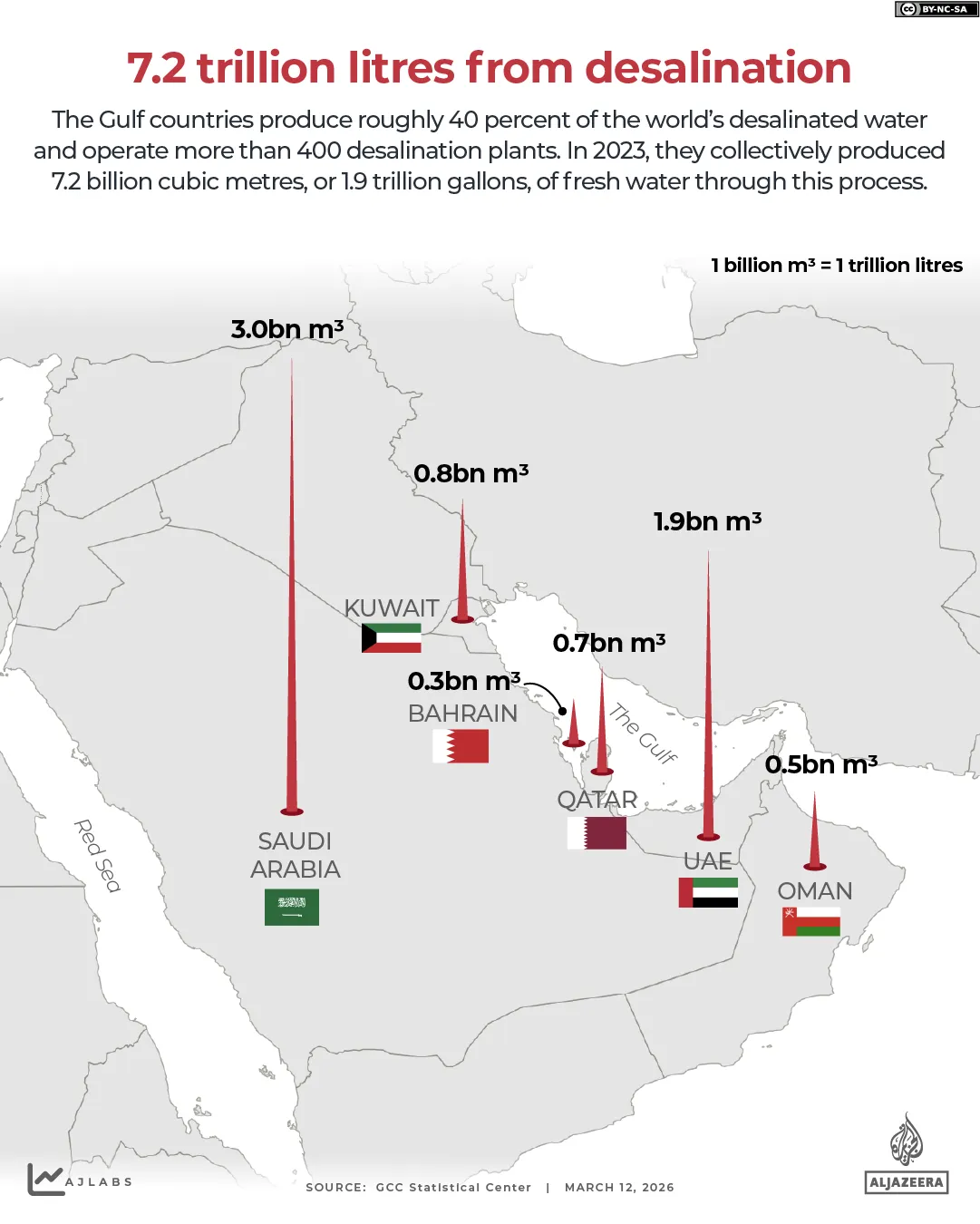

The Gulf region is responsible for approximately 40 percent of global desalinated water production, with over 400 operational desalination facilities distributed along its coastlines. According to the United Nations, the benchmark for absolute water scarcity is defined as less than 500 cubic metres (655 cubic yards) of renewable freshwater resources per capita per year. In comparison, the Gulf states possess an average per-capita endowment of only about 120 cubic metres (155 cubic yards) of natural freshwater annually, positioning them well below this threshold.

Consequently, desalination has become a cornerstone of water security strategies across the region.

Here is an illustration of the numbers across the Gulf countries.

On a per-capita basis, this output corresponds to roughly 122 cubic metres annually, or about 334 litres (88 gallons) per day.

Notably, the installed desalination capacity of these states exceeds actual production, estimated at around 26.4 billion cubic metres per year.

Within the region, Saudi Arabia—the largest and most populous Gulf state with a population of approximately 37 million—accounted for the highest share of desalinated water production, generating 3 billion cubic metres in 2023. It was followed by the United Arab Emirates with 1.9 billion cubic metres, Kuwait with 0.8 billion cubic metres, Qatar with 0.7 billion cubic metres, Oman with 0.5 billion cubic metres, and Bahrain with 0.3 billion cubic metres.

But food insecurity is only one layer of the crisis. Water is arguably more acute. CFR's Werz documents the stark vulnerability:

Water is also of concern. The first Iranian attacks on desalination plants in Bahrain and strikes landing close to a massive complex with forty-three desalination plants in Saudia Arabia indicate yet another layer of strategic warfare. The entire Gulf region is extraordinarily dependent on desalination technology with four hundred plants in the GCC member states producing almost 40 percent of global desalinated water. In Kuwait, 90 percent of the drinking water depends on these plants, 86 percent in Oman, and 70 percent in Saudi Arabia. In total, 100 million people in the region rely on these water sources. A leaked 2008 cable sent from the U.S. Embassy in Riyadh documented that one desalination plant supplied over 90 percent of Riyadh’s drinking water and stated that the city “would have to evacuate within a week” if the plant, its pipelines, or associated power infrastructure were seriously damaged or destroyed. Political leaders in the region understood back then that water was (and is) more important than oil to the national well-being. Today, Saudi Arabia is even more dependent on desalination plants. Energy-intensive technology provides almost three-quarters of its drinking water. (Source: The Iran War’s Hidden Front: Food, Water, and Fertilizer / Council on Foreign Relations)

A 2008 U.S. Embassy cable from Riyadh, later disclosed by WikiLeaks, concluded that Riyadh "would have to evacuate within a week" if its primary desalination plant were seriously damaged. The city now has seven million residents. The strategic exposure has only grown.

In 2008, a diplomatic cable sent from the U.S. Embassy in the Saudi capital, Riyadh, and later released by WikiLeaks warned that a single desalination plant provided Riyadh with more than 90 percent of its drinking water at the time. The city “would have to evacuate within a week if the plant, its pipelines or associated power infrastructure were seriously damaged or destroyed,” the author wrote. “The current structure of the Saudi government could not exist” without the plant, the cable added. (Source: Vital Water Desalination Plants in Iran and Bahrain Are Attacked / New York Times)

Iranian strikes have already targeted desalination infrastructure in Bahrain and landed near major Saudi facilities. This is not random targeting. It is a deliberate strategic message about the limits of Gulf civilian resilience — a form of coercive signaling that makes the food-water double vulnerability into a strategic weapon.

Making Desalination Plants Dysfunctional

Disabling a desalination system does not always require the physical destruction of its main structures. Targeting the plant’s vulnerabilities—particularly its seawater intake, energy supply, and distribution network—can be sufficient to interrupt potable water production for large populations.

The use of a radiological dispersal device (“dirty bomb”) in Gulf waters would pose an additional, more complex threat. Desalination processes such as reverse osmosis can remove many radioactive contaminants, but not with absolute reliability, and membrane performance may degrade under sustained exposure.

Depending on radionuclide types, concentrations, and dispersion, authorities might suspend operations, reconfigure intake locations, or add specialized treatment before resuming supply.

Thus, while a single radiological incident would not automatically make desalination permanently impossible, it could compel extended shutdowns or capacity reductions, with severe humanitarian and strategic consequences for highly dependent Gulf states.

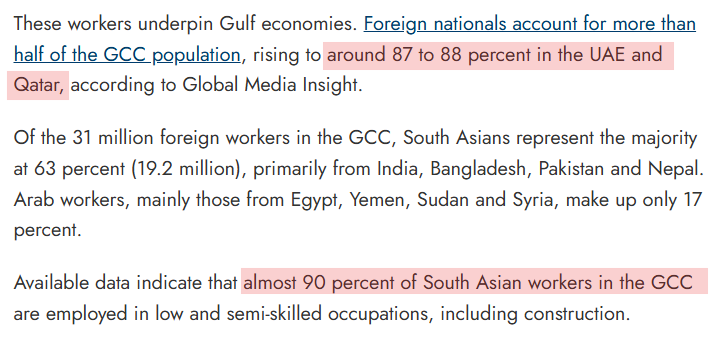

Thirty-One Million Workers: The Human Architecture of Gulf Civilization

The question of whether the GCC can become ungovernable if its migrant workforce leaves is not hypothetical. It is an empirical question with a measurable threshold, and we are already moving toward it.

The scale of dependency is total and underappreciated in most Western commentary.

AGBI's Chatham House fellow Neil Quilliam documents the structure of the workforce with precision:

These workers are not peripheral. They are the operational substrate of Gulf civilization — running the ports, construction sites, logistics networks, hospital wards, power-plant maintenance crews, desalination plant operations, and food warehouses. Gulf citizens largely hold government, military, supervisory, and professional roles. The physical economy runs on South Asian labor.

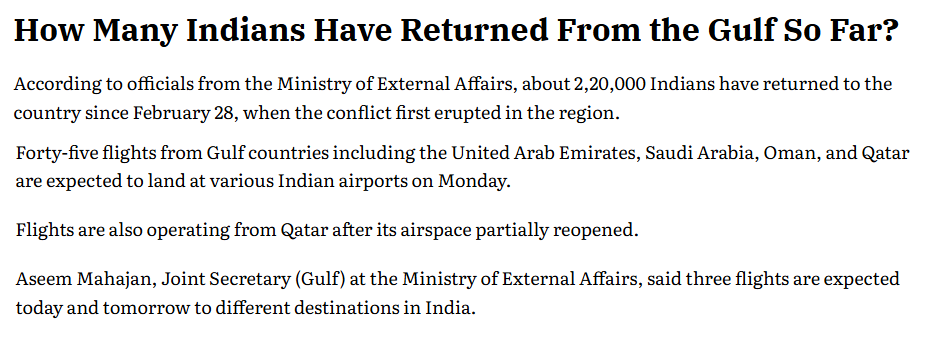

The departure has already begun. As of mid-March, over 220,000 Indian nationals had been repatriated from the GCC and Iran — and critically, this reverse migration includes a disproportionate share of skilled professionals and business owners, not just day laborers. The human capital embedded in complex operations is being hollowed out alongside the manual workforce.

Quilliam draws the historical comparison starkly: "migrant workers were the first to face repatriation during the financial crisis of 2008 and during the Covid era, when more than 1 million workers returned home, including 700,000 from India alone." But both those crises lacked kinetic threats to urban infrastructure.

Yale's Mushfiq Mobarak identified what is perhaps the most consequential and underreported impact of the war.

The Gulf labor model, as Quilliam concludes, "supports rapid expansion in good times, but it also allows costs to be cut quickly when conditions change." The direction of that adjustment is now visible and accelerating.

India: Racing the Monsoon

India's situation has a temporal urgency not fully captured in mainstream coverage. The challenge is not merely whether fertilizer is available today — it is whether it reaches farmers in the right form, at the right price, in the right locations, before June, when the southwest monsoon arrives and the kharif planting season begins.

India consumes approximately 35–36 million tonnes of urea annually and produces around 28–29 million tonnes domestically. The gap is normally covered by Gulf imports.

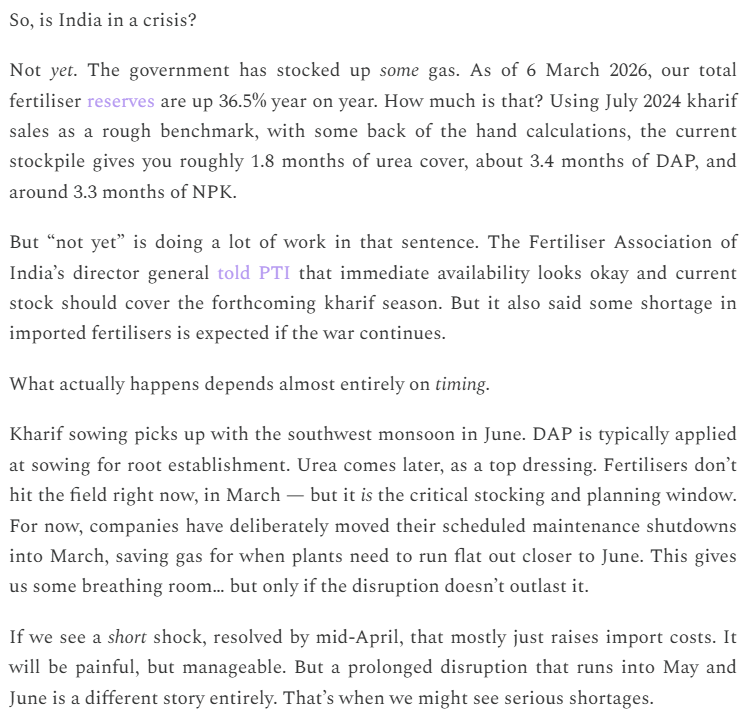

That channel is now severed. India had approximately 6.2 million tonnes of urea in stock as of mid-March — enough to cover roughly 1.8 months of normal consumption, providing a buffer until approximately mid-May. After that, new supplies must arrive, or rationing begins in earnest.

The Daily Brief's analysis of what happens at the plant level is worth quoting precisely because it illustrates how supply chain disruption translates into food production risk:

"Kharif sowing picks up with the southwest monsoon in June. DAP is typically applied at sowing for root establishment. Urea comes later, as a top dressing."

The timing dependency is absolute. If fertilizer does not arrive before June, the damage to the harvest is locked in regardless of what happens afterward.

The government is seeking emergency supplies from Russia, Belarus, Morocco, and even attempting to negotiate with China to ease export restrictions (Source: Reuters) — a request that reflects both the severity of the situation and the extent to which geopolitical compulsions have been set aside under agricultural necessity.

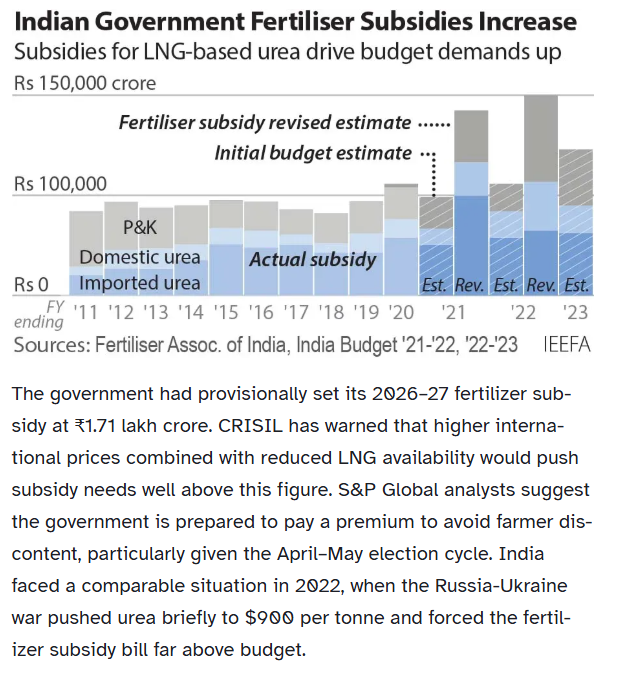

The fiscal dimension compounds the operational one. India's provisionally budgeted fertilizer subsidy for 2026–27 was ₹1.71 lakh crore (Source: PIB)— already stretched before the war.

CRISIL has cautioned that a mix of elevated global prices and tighter LNG supplies could drive India’s fertilizer subsidy requirement far beyond current projections. In effect, the budgeted outlay may prove significantly understated if present trends persist.

A similar pattern played out in 2022, when international urea prices briefly approached about 900 dollars per tonne, blowing a substantial hole in the planned subsidy allocation. That episode exposed how quickly external price shocks can destabilize fiscal calculations in a sector so dependent on imported inputs, and it underpins today’s warnings about renewed pressure on the subsidy bill.

India's long-term strategic response — a major fertilizer production facility under joint development with Russia — was precisely the right geopolitical instinct. But it is not yet operational. It will not resolve this crisis. It is the answer to the next one, assuming the political will to see it through survives the turbulence of the current moment.

Brazil: Agricultural Superpower with a Gulf Dependency

Brazil's agricultural achievement is one of modern civilization's most underappreciated stories. The transformation of the Cerrado savanna into the world's most productive soybean and corn landscape was accomplished through a combination of tropical agronomy, infrastructure investment, and industrial fertilizer application at enormous scale. Brazil now feeds significant portions of Asia and Europe.

It is also the world's largest importer of fertilizer, having consumed roughly 49 million metric tons in 2025, with key suppliers in the Middle East.

Brazil imported about 49.11 million metric tons of fertilizer in 2025, making it the world’s largest importer of fertilizer, with key suppliers in the Middle East. Although Brazilian officials have noted that the country is well positioned to weather short-term disruptions, any prolonged disruption to production or shipping in the region could tighten fertilizer availability and raise costs for Brazilian farmers. (Source: Chokepoint: How the War with Iran Threatens Global Food Security / CSIS)

The dependency chain runs directly through the Gulf: Middle Eastern urea flows to the Brazilian interior, where it is applied to fields that export soybeans to China to feed the livestock sustaining China's urban protein consumption. This supply chain is extraordinarily long, and it now has a broken link.

To be clear, about half of fertilizer is not traded internationally at all. The United States, a land of abundant natural gas, produces about three-quarters of the fertilizer it consumes, while China is even more self-sufficient. But because these are globally traded commodities, problems in one place ripple throughout the global economy. Even before the war in Iran, China was restricting fertilizer exports to protect its own farmers—but it needs Brazil, which is highly dependent on Middle Eastern urea, to be able to grow soybeans to feed to the pigs and cows in both countries. (Source: The Other Global Crisis Stemming From the Strait of Hormuz’s Blockage / CSIS)

Chinese food security — treated by the Politburo as a core sovereignty issue — has a critical external node in the Brazilian interior, which in turn has a critical input dependency on the Middle East. The Hormuz closure is, through this chain, also a partial threat to Chinese food supply stability.

There is an additional dynamic that biofuel economics introduces. When oil prices surge — as they have, with crude crossing $100 per barrel — ethanol and biodiesel become dramatically more profitable.

Brazilian cane mills are already shifting toward ethanol rather than sugar, and soybean oil futures hit their highest level in two and a half years within the war's first week.

China: The Self-Insured Superpower and Its Strategic Calculus

China has, through decades of deliberate agricultural policy, built a degree of fertilizer self-sufficiency that no other large economy has achieved. It is the world's largest producer of both nitrogen and phosphate fertilizers, and it maintained export restrictions on both even before the Iran war to ensure domestic supply adequacy.

This self-insurance means China is far less directly exposed to the Hormuz fertilizer shock than India, Bangladesh, or Egypt. Its farmers will plant on schedule. Its food prices, while affected by global spillover and by disruption to its Middle Eastern LNG imports, will not see the supply-side collapse that confronts lower-income importers.

But China's role in the crisis is significant precisely because of what it chooses to do with its surplus production capacity. China’s phosphate export curbs are currently scheduled to end in August this year, a move that could boost global supply. However, given the recent market volatility, there is a strong possibility that Beijing may choose to prolong these restrictions rather than ease them.

China is unlikely to relax its phosphate fertilizer export suspension, despite the war in the Middle East, with multiple traders and producers saying on March 3-4 that the policy is tied to domestic priorities rather than short-term geopolitical developments. (Source: China to maintain phosphate export suspension despite Middle East war / S&P Global)

Not just phosphates, the Chinese restrictions will play out in other fertilizers as well.

The global price spike creates arbitrage incentives that Beijing worries could draw domestic supplies toward export, raising Chinese domestic prices — precisely the political outcome the Politburo will not tolerate.

China's export restrictions remain firmly in place, and there is little pressure on Beijing to change that. What China may do — selectively, bilaterally, and on its own terms — is to offer targeted access to fertilizer to strategically important partners, converting scarcity into leverage.

Russia: The Accidental Agricultural Hegemon

Russia has entered the current crisis from a structurally complex position. It is one of the world’s largest fertilizer producers, accounting for roughly one-fifth of global trade, yet it remains constrained by sanctions, limited access to Western markets, and production systems already operating near capacity. At the same time, it has become the most viable large-scale alternative supplier for countries seeking to replace disrupted Gulf exports.

The global supply landscape offers few substitutes. China’s exports are constrained by domestic policy priorities, while other producers, such as Morocco and Indonesia, lack the scale to offset a major supply gap. As a result, countries that spent recent years reducing dependence on Russian fertilizers are now reversing course. India has begun engaging Russia and Belarus for emergency supplies. European importers, after years of deliberate diversification, are confronting the reality that equivalent alternative capacity was never developed. Similar dynamics are visible across Turkey, Egypt, Bangladesh, and parts of Africa.

Russia’s ability to expand supply exists but is constrained. Domestic demand pressures, infrastructure limitations, and disruptions to production facilities constrain the additional volume that can be brought to market. In this context, allocation becomes strategic rather than purely commercial. Supply flows are increasingly shaped by geopolitical alignment, with preference given to neutral or friendly states, while those aligned against Moscow face reduced access.

The broader implication is a structural shift in global agricultural dependency. Just as earlier crises reconfigured energy flows, the current disruption is reshaping fertilizer and food supply chains. Russia’s combined position as a leading fertilizer producer, grain exporter, and energy supplier places it at the center of this emerging system.

This influence is not temporary; it reflects a deeper realignment that is likely to persist beyond the immediate crisis.

Southeast Asia, the Philippines, and the Remittance Channel

Southeast Asia encounters the food shock of the Iran conflict through three interconnected channels that are often examined in isolation:

- rising energy costs feeding domestic food inflation,

- fertilizer price transmission into agricultural production, and the

- destabilizing effects of disrupted migrant labor flows from the Gulf.

The first two channels converge in the region’s core agricultural economies—Vietnam, Thailand, Indonesia, and the Philippines—all of which depend heavily on rice cultivation. Modern paddy farming is highly nitrogen-intensive, with urea as a critical input. A sharp increase of over 40 percent in urea prices has significantly altered farmers' cost structure.

Since late February, disruptions to the Strait of Hormuz have sent nitrogen and phosphate prices soaring. Nitrogen fertilizer prices, in particular, have surged globally. Platts assessed FOB Middle East granular urea at $604-$710/mt on March 19, a sharp jump from $436-$494/mt on Feb. 26 before the conflict began. The Southeast Asia granular urea price was $750/mt FOB on March 19, up from $490-$498/mt pre-conflict. While still under upward pressure, it is below the highs of 2022, and this increase puts prices firmly above levels seen since 2023. (Source: S&P Global)

Smallholders in regions such as the Mekong Delta or Mindanao operate with thin margins and limited access to credit. (Source: Financial Times)

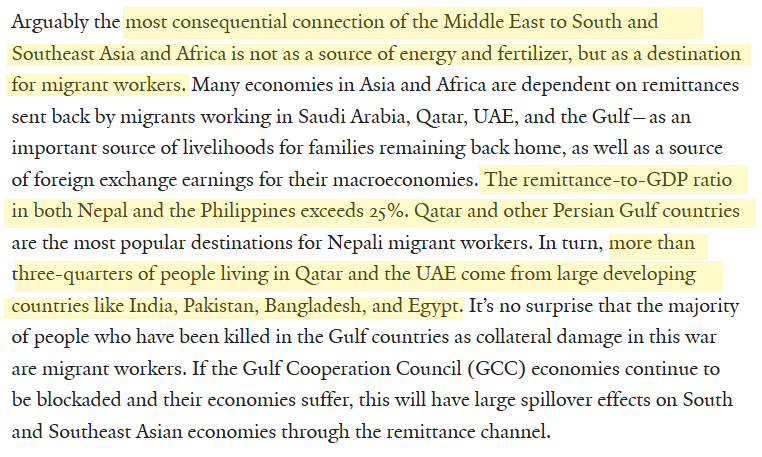

The third channel: remittances is less visible but equally consequential. In countries like the Philippines and Nepal, remittance inflows account for more than 25 percent of GDP.

Meanwhile, with remittances from OFWs making up nearly 10% of the Philippines GDP at $38 billion, there is little incentive for the government to stop its decades-long business of exporting its people to work abroad, Conception said. For countries such as Nepal, which also sends hundreds of thousands of migrant workers to the Gulf region, remittances can make up over 26%, according to The World Bank. (Source: NPR)

Household consumption, education, and local economic activity are closely tied to income earned by migrant workers in the Gulf. Disruptions to employment, whether due to conflict, mobility restrictions, or forced returns, transmit rapidly back to domestic economies. The loss of income is not gradual; it is immediate and deeply felt at the household level.

The human dimension underscores the severity of this channel. Early in the conflict, a Filipino migrant worker was killed in a missile strike, highlighting the direct exposure of overseas labor to geopolitical risk. With evacuation constrained and uncertainty rising, governments face an impossible dilemma: leaving workers in place exposes them to danger, while mass repatriation risks overwhelming already fragile domestic economies.

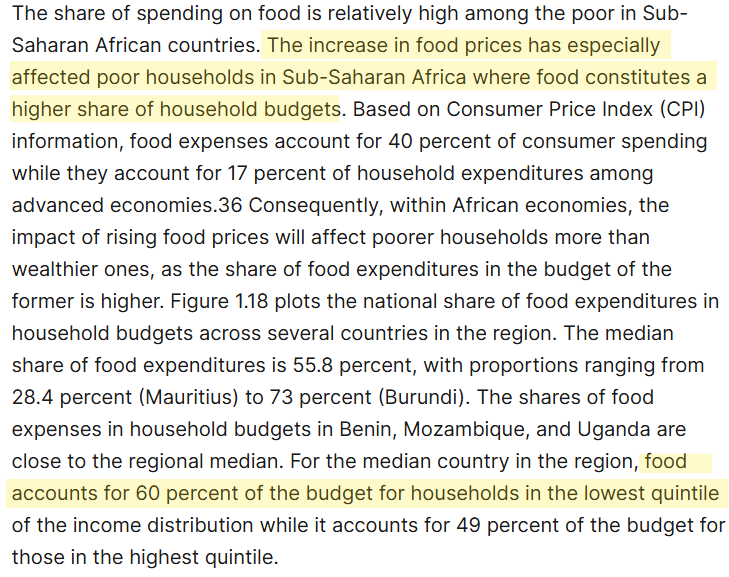

Africa: Where Food Price Shock Becomes Famine

Food crises do not distribute their effects evenly.

The same percentage increase in global prices produces radically different outcomes depending on household income structures.

This asymmetry becomes most dangerous in regions where large populations already live at the edge of food insecurity. In parts of Sub-Saharan Africa, the underlying arithmetic turns a price shock into a humanitarian emergency. Fertilizer disruptions in recent years have already weakened agricultural productivity in key economies such as Côte d’Ivoire, Kenya, Nigeria, and South Africa. With limited recovery since then, these systems now face a second, larger shock layered onto an already fragile base.

As of July 2025, more than 307 million Africans—over 20 per cent of the continent’s population—are affected by hunger. Childhood stunting averages 30.7 per cent across Africa, with wasting (insufficient weight relative to a child’s age) at 6 per cent. In some countries, one in three children is malnourished. Somalia has the highest rates, but Chad, Zambia, Uganda, Kenya, and Guinea-Bissau also exceed 30 per cent undernourishment. (Source: Confronting alarming food insecurity trends in Africa: An expert’s view / IFRC)

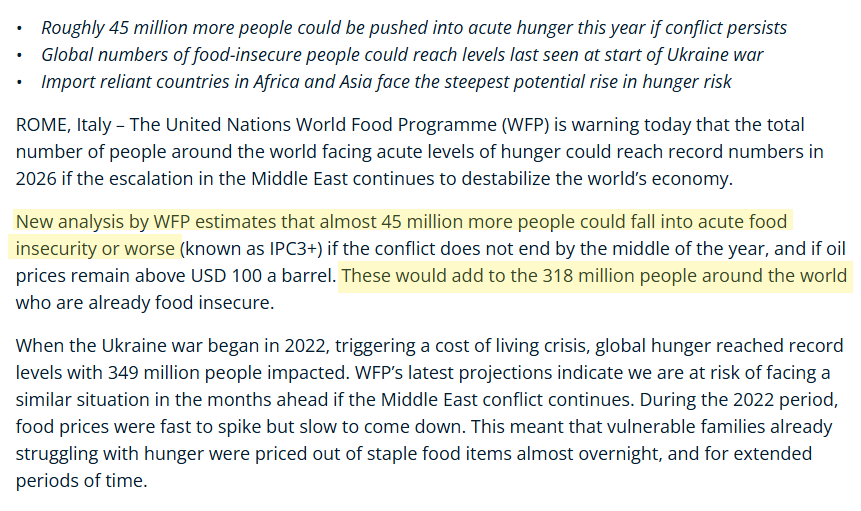

The global context is equally stark. Even before the current escalation, more than 670 million people—over 8 percent of the world’s population—were experiencing chronic hunger. Active famine conditions were already present in multiple regions, leaving no buffer to absorb further disruptions.

Current projections indicate that an additional 45 million people could be pushed into acute food insecurity, raising the global total to approximately 363 million. In reality, this number is likely conservative, given the cascading effects of supply constraints, currency pressures, and political instability.

The consequences extend far beyond immediate hunger. Short periods of nutritional deprivation during childhood can have irreversible effects on cognitive development and physical health. These impacts reduce lifetime productivity, weaken human capital formation, and entrench poverty across generations. In this sense, food crises are not just episodes of scarcity; they are mechanisms of long-term structural damage. They reshape societies by limiting the potential of those who survive, ensuring that the effects of a single shock echo for decades.

The United States: Absorbing the Costs of Its Own War

The United States remains broadly self-sufficient in caloric production, yet this apparent strength conceals a deeper vulnerability: its agricultural system is tightly coupled to global fertilizer markets. Disruptions in these markets—especially during periods of geopolitical conflict—can rapidly ripple through domestic cost structures, exposing farmers and consumers alike to significant economic strain.

Recent movements in fertilizer prices illustrate the scale of the problem. Urea, a critical nitrogen input, has experienced a sharp price escalation within a short span, dramatically altering the input-output economics of American farming. Where fertilizer once represented a manageable share of crop value, it now consumes a far larger share of expected returns. This shift compresses farm margins and introduces heightened uncertainty into planting decisions.

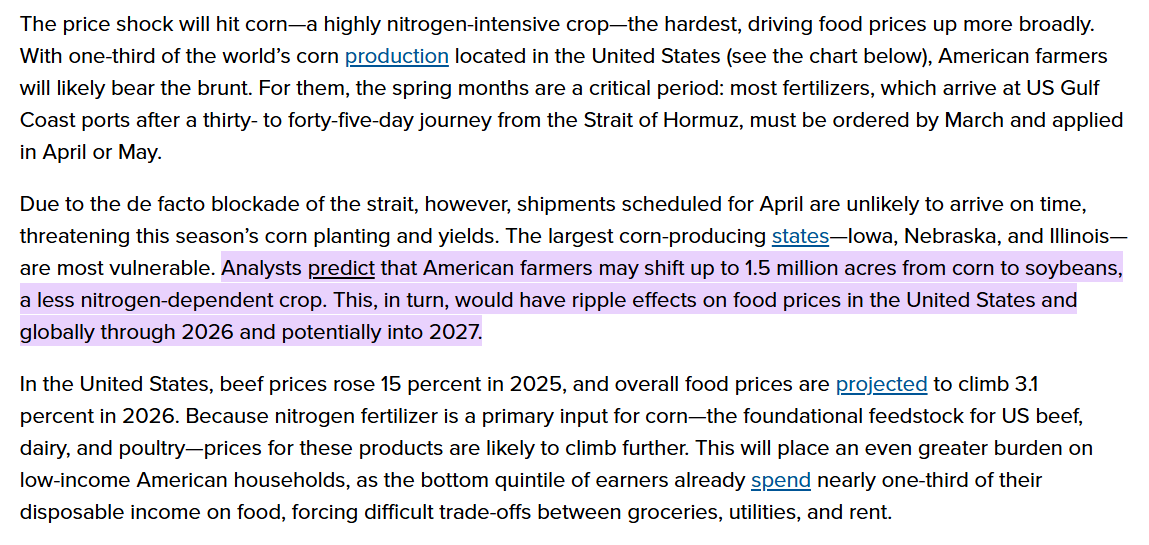

A significant shift away from fertilizer-intensive crops, particularly corn, towards alternatives such as soybeans is projected for the 2026 planting season, driven by surging fertilizer costs and tighter operating margins.

Because soybeans can fix their own nitrogen through natural biological processes, they are becoming a more attractive option for farmers looking to reduce the high input costs associated with nitrogen-hungry corn.

While economically sensible at the individual level, this transition carries systemic consequences. Reduced corn acreage can tighten supply, driving up prices not only for staple grains but also for livestock feed and biofuel inputs. The ripple effects extend through the food system, ultimately manifesting as higher prices for meat, dairy, and processed goods.

The broader implication is that once triggered, food inflation becomes politically consequential. In an environment where input costs are volatile and supply adjustments lag demand, price pressures can persist and intensify. For a nation deeply integrated into global agricultural and energy systems, the strategic risks are not confined to production capacity alone. They lie in the intersection of market exposure, policy choices, and the delayed but powerful feedback loops of inflation.

The Irreversibility Problem: Why Ceasefire Is Not the Solution

This is the analytical crux that the geopolitical commentary has systematically failed to foreground: a ceasefire signed tomorrow would not solve the food crisis. The famine machine, once activated, runs on a calendar that is independent of diplomatic outcomes.

Carnegie's Gordon and Corthell state the core problem directly: "restarting production and transport for fertilizers and their components could take weeks — weeks that Northern Hemisphere farmers do not have." (Source: Carnegie Endowment)

But the weeks problem is actually the optimistic framing. The deeper problem is that the decisions that determine this year's harvest have already been made — or are being made right now, under conditions of price uncertainty and supply scarcity. Fields under-fertilized in April do not produce smaller harvests in April. They produce smaller harvests in September and October. Food price consequences arrive in grocery stores in November and December, and persist through 2027.

CNBC's reporting on analyst sentiment captures the scale of expert alarm. One fund manager told CNBC:

"I'm a lot more concerned about the current crisis than I was when Russia-Ukraine happened four years ago." (Source: CNBC)

His reasoning is structural: "It could really have an impact on agricultural yields across a lot of geographies, and across the major crops such as maize."

Unlike in 2022, when buffer stocks of food commodities provided partial insulation, the current shock hits multiple producing regions simultaneously and arrives at the worst possible moment in the planting calendar.

The asymmetry between crisis creation and crisis resolution is therefore profound.

Russia, Turkey, and the New Overland Geographies of Food

One structural consequence of the Hormuz closure that will outlast the war itself is the accelerated emergence of overland trade corridors through Russia, Turkey, and Central Asia as the functional backbone of food and fertilizer supply for the Middle East and North Africa.

CFR's Werz identifies this realignment explicitly: "new overland transport corridors will open, putting Russia, Turkey, and Syria in a position of strategic control over vital supplies."

Turkey sits at the junction of European, Central Asian, and Middle Eastern trade routes, with the port infrastructure and logistics networks to function as a genuine commodity hub. Countries that become dependent on Russian-controlled overland fertilizer supply, or on Turkish redistribution facilities, will find that dependency difficult to reverse even after Hormuz reopens.

The strategic irony is not subtle. The United States and Israel launched a war intended to reshape the Middle East's power architecture. One of its structural consequences is accelerating Eurasian overland trade integration — strengthening precisely the Russian and Turkish positions that Western policy has sought to constrain for a decade.

The Systemic Lesson: Strategic Reserves and What Comes Next

Every major geopolitical shock produces a lesson. The lesson of this crisis is becoming impossible to avoid: food security infrastructure — fertilizer production capacity, strategic input reserves, supply chain diversification — must be treated as strategic national security infrastructure on par with energy reserves and defense capability.

The United States maintains a Strategic Petroleum Reserve because the 1973 oil crisis taught it that energy dependence was a strategic vulnerability. It does not maintain an equivalent strategic fertilizer reserve, because no one legislated the lesson from 1973 into agricultural policy. The G7 countries have collectively failed to build the institutional mechanisms — emergency fertilizer stockpiles, diversified supply chain agreements, humanitarian input reserves — that could blunt a shock of this kind.

Because fertilizer has less value than oil and gas, political and business leaders expend fewer resources to make sure it keeps flowing. A ship captain bold enough to brave drone strikes and dash through the Strait of Hormuz would prefer to carry oil than fertilizer, a preference that would be shared by any potential navy escort, which the United States is in any case not yet able to provide. G7 countries don’t maintain strategic fertilizer reserves to match their oil stockpiles. The pipeline that Saudi Arabia built to enable exports through the Red Sea rather than the Strait of Hormuz is for oil, not ammonia products. (Source: The Other Global Crisis Stemming From the Strait of Hormuz’s Blockage / Carnegie Endowment)

The medium-term agenda is clear even if its political economy is difficult. Nations need strategic fertilizer reserves comparable to their petroleum reserves. Humanitarian organizations need guaranteed access to pre-positioned agricultural input stocks in crisis-prone regions.

Supply chain diversification — India's investment in a Russian fertilizer plant is one concrete example — needs to become an explicit strategic priority rather than a reactive afterthought.

The Planting Season Does Not Wait

The Iran war is being analyzed primarily as an energy crisis, a regional power contest, a test of the nuclear nonproliferation regime, and a moment of divergence between the United States and Israel. All of these frames are real. None of them is the frame through which its deepest consequences will ultimately be measured.

The deepest consequences will be measured in harvests. In the kharif planting season, which Indian farmers begin in June. In the Sahel's agricultural output in September. In the food prices Egyptian, Bangladeshi, and Filipino urban households pay in November. In the WFP emergency appeal numbers for 2027. In the political stability of governments whose legitimacy rests on affordable bread.

This draws back to Iran, where the systematic weaponization of food, water, and fertilizer in a thirsty region makes this the first true twenty-first-century conflict that could unleash a slow-motion famine machine. Water and food aren’t humanitarian concerns at the periphery of the conflict but—given the thin margin of error when it comes to functioning water and food supply in the region—are rapidly becoming the conflict’s most consequential terrain. At scale, the war-driven fertilizer shock combined with climate-stressed growing seasons, depleted grain reserves, and debt-constrained governments should be considered a threat to the world at large. If left unaddressed, it has the potential to convert a regional military conflict into a global humanitarian crisis. (Source: The Iran War’s Hidden Front: Food, Water, and Fertilizer / CFR)

The Gulf states face an existential test of the social contract they have built over fifty years of hydrocarbon abundance — tested simultaneously by food, water, and the labor force that makes their cities function.

Comments ()