When game playing the future, one set of variables - economic or technological or geopolitical or religious/ideological - are tough enough.

Currently, with wars, technologies and religious ideologies on the brink, we are looking at an economic fallout as well.

Where are we headed?

We discussed the apprehensions we have with the AI disobeying humans and the direction it has taken on our YouTube channel. Please check that out.

Today we will evaluate the economic situation while adding other variables that will impact the economic factors further.

Please share your comments and thoughts with us.

SUPPORT DRISHTIKONE

In an increasingly complex and shifting world, thoughtful analysis is rare and essential. At Drishtikone, we dedicate hundreds of dollars and hours each month to producing deep, independent insights on geopolitics, culture, and global trends. Our work is rigorous, fearless, and free from advertising and external influence, sustained solely by the support of readers like you. For over two decades, Drishtikone has remained a one-person labor of commitment: no staff, no corporate funding — just a deep belief in the importance of perspective, truth, and analysis. If our work helps you better understand the forces shaping our world, we invite you to support it with your contribution by subscribing to the paid version or a one-time gift. Your support directly fuels independent thinking. To contribute, choose the USD equivalent amount you are comfortable with in your own currency. You can head to the Contribute page and use Stripe or PayPal to make a contribution.

Economies in Trouble

We may not realize easily because its not always in the news but there is an exodus of the super-rich from London.

This points to the capital flight in response to perceived increases in risk and diminishing returns.

Reports are now indicating that over 11,000 millionaires are anticipated to leave London in 2024 alone, with many redirecting their wealth towards destinations in Asia and North America.

This migration is attributed to a confluence of factors, including

- the UK's high tax burden—exacerbated by the abolition of the non-domiciled (non-dom) tax status

- the lingering economic repercussions of Brexit, and

- a broader perception that the UK is becoming a less favorable environment for wealth.

Consequently, London has reportedly slipped out of the top five wealthiest cities globally.

This phenomenon is significant beyond its impact on the UK; it highlights a sensitivity of global capital to changes in taxation, economic stability, and a nation's perceived standing in the global financial order.

These movements will start influencing global capital flows and overall investor sentiment.

London has long been a magnet for the global rich. Oligarchs, leaders in exile, hedge fund managers and high-net-worth locals coexist in a city where old and new money collide. The global elite are drawn to the British capital for its legal and professional services, top schools, cultural offerings, high-end real estate and of course, for English, a global language for business. But there are growing signs — met with a shrug or even relief in some quarters — that some of U.K.’s very richest residents are decamping to countries like Spain, Italy, Switzerland and the United Arab Emirates, places where taxes are lower or where the rich can pay a flat tax to shield their global income. (Source: "Are the super-rich leaving London? Tax changes could spur wealth exodus." / MSN)

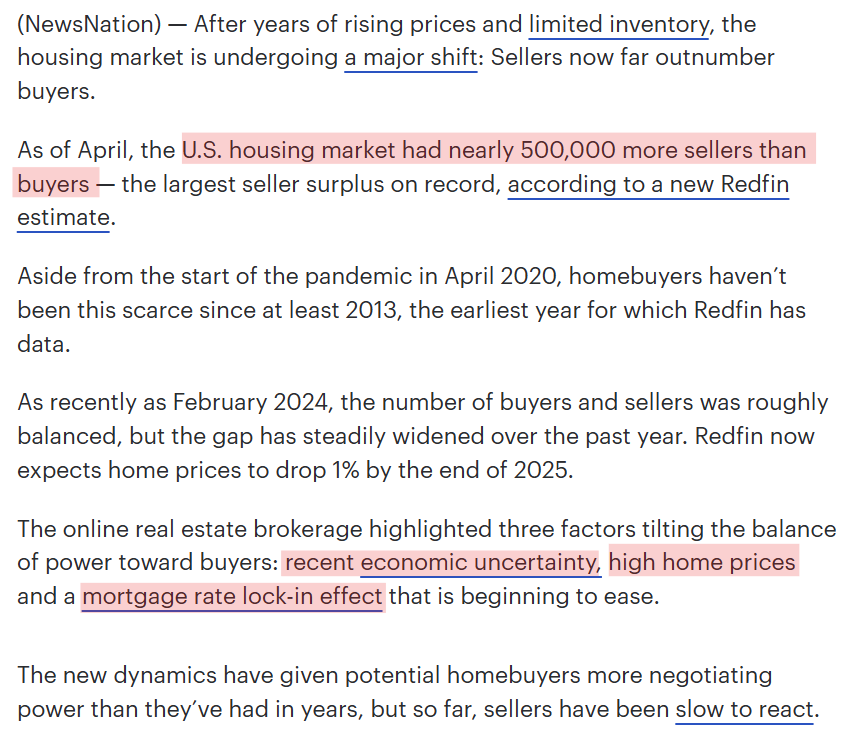

Meanwhile, as of April 2025, the U.S. housing market is facing its most significant imbalance in over a decade.

According to Redfin, there are nearly 500,000 more home sellers than buyers, with sellers outpacing buyers by 34%—the widest gap since 2013. This marks a dramatic reversal from just two years ago, when buyer demand dominated the market.

Such a pronounced mismatch between supply and demand typically points to an impending market correction.

Falling home prices wipe oout household wealth and hit consumer confidence, both critical drivers of economic momentum.

Redfin expects U.S. home prices to drop 1% by year-end, with declines already underway in cities like Dallas, Oakland, and Jacksonville.

The way home prices have risen in the past couple of years, the houses have become unaffordable. Just check this -

So the real estate may on its way down in the coming months.

Bond Markets in Turmoil

During the global financial recalibration, the bond market of the world’s third-largest economy is sounding alarms.

Japan, known for monetary discipline and investor predictability, is witnessing a dramatic unraveling in demand for its long-term sovereign debt.

Beneath the surface of falling auction ratios and rising yields may lie a story of shifting paradigms.

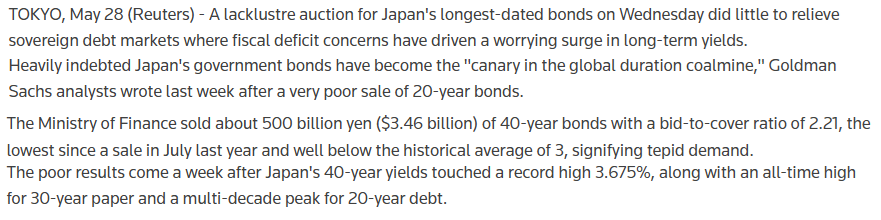

On May 20, 2025, Japan’s 20-year government bond (JGB) auction recorded a bid-to-cover ratio at its lowest since 2012.

In simple terms, demand is drying up. Even more telling is the widening “tail”—the spread between the average and lowest accepted prices—which betrays investor reluctance, a silent vote of no confidence in the pricing, and perhaps, the issuer.

The 40-year bonds have fared no better. Once the symbol of Japan’s fiscal endurance and trust in long-term planning, these ultra-long bonds are now increasingly being met with skepticism. A market once fueled by certainty is now haunted by hesitation.

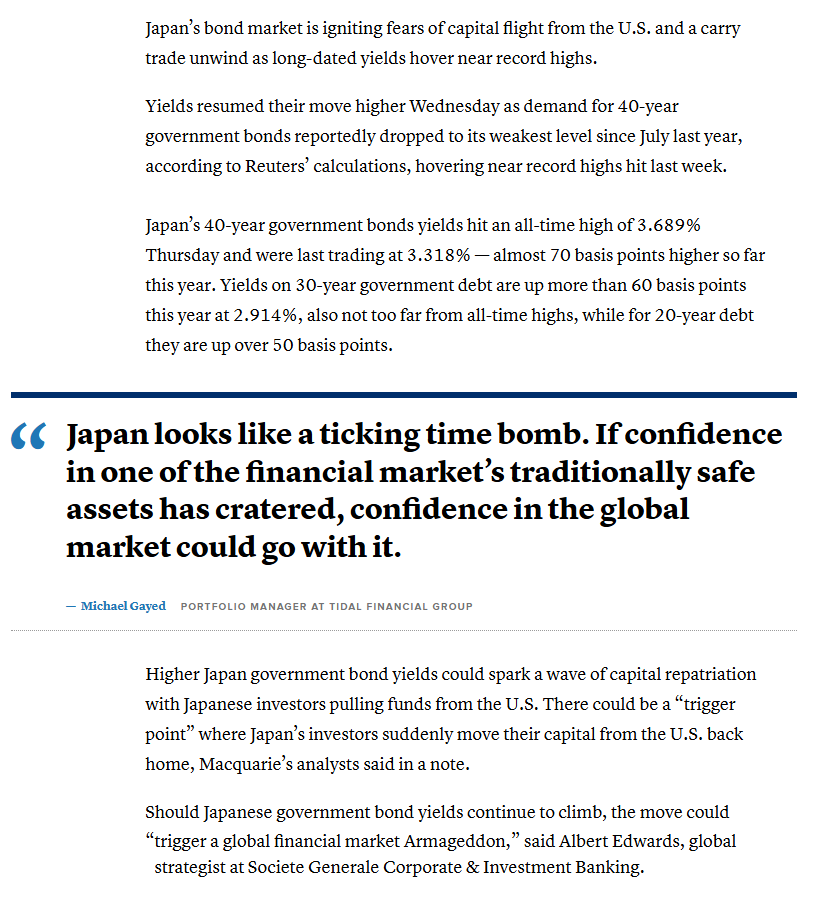

This decline in appetite for long-term Japanese Government Bonds (JGBs) has led to rising yields, with 40-year yields reaching 3.675%, the highest on record.

So what does that mean?

The rise in domestic yields will push Japanese investors to repatriate funds previously invested in foreign assets, such as U.S. Treasuries. That could impact the global financial markets in a big way.

We could be looking at potential unwinding of the "yen carry trade," where investors borrow in low-interest yen to invest in higher-yielding assets abroad.

And, this could lead to increased volatility in global bond and equity markets.

The rising JGB yields could be because of:

- Bank of Japan's Policy Shift: The BoJ has been reducing its bond purchases, moving away from its long-standing quantitative easing program, thereby allowing yields to rise as bond prices fall.

- Inflationary Pressures: Persistent inflation in Japan reduces the attractiveness of fixed-income assets, especially those with low yields.

- Fiscal Concerns: Japan's public debt exceeds 250% of GDP, raising sustainability concerns and consequently increasing borrowing costs.

Meanwhile, Japan's Ministry of Finance is considering reducing the issuance of super-long-term bonds to alleviate upward pressure on yields.

Needless to say, today we are witnessing how the global financial system is interconnected, and as a result, domestic policy changes can have far-reaching international effects.

It's not just the Japanese market that's impacted. So is the US bonds market.

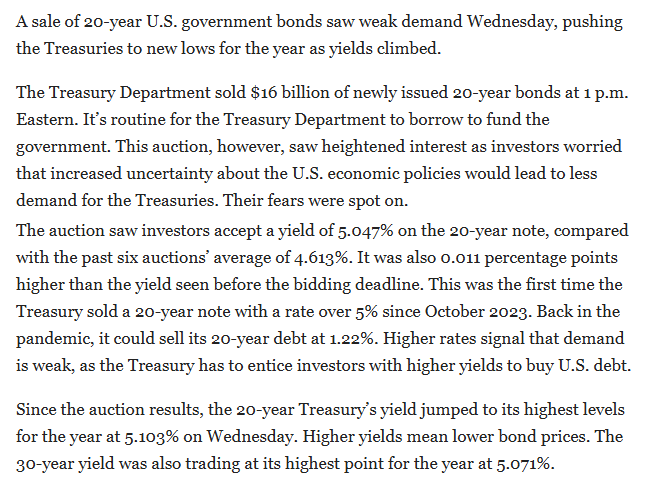

In the spring of 2025, the U.S. Treasury bond market showed signs of strain, but not collapse.

That may have changed in May 2025, when a 20-year Treasury auction yielded higher-than-expected returns to investors. This reflected weaker demand, as the government was forced to offer more attractive terms—higher yields and thus lower prices—to entice buyers.

This auction was not an isolated event but part of a broader pattern of investor caution.

Still, the situation was far from a crisis. While yields temporarily spiked, they soon stabilized, suggesting that investor appetite remained fundamentally intact. Despite headlines forecasting turmoil, the underlying demand for Treasuries remained solid, bolstered by their status as essential assets in global portfolios, which offer both income and security.

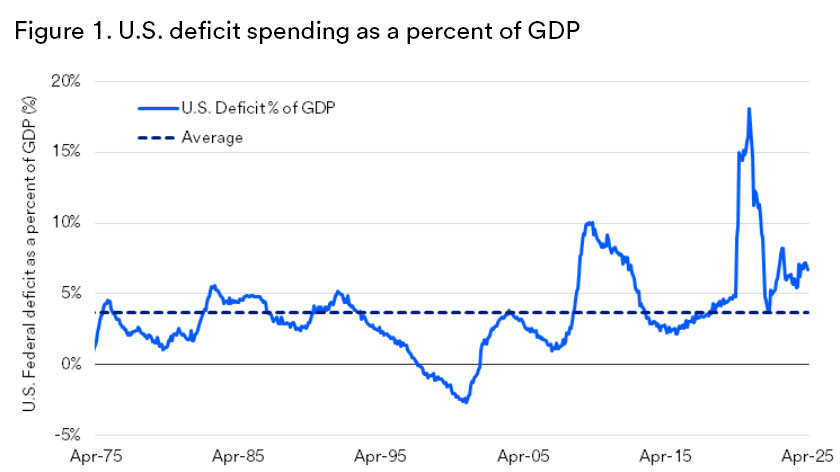

Critics also pointed to America’s high deficit spending as a long-term concern for bond investors, fearing it could eventually push yields higher and inflate borrowing costs.

Let's be clear - the high deficit figure—7% of U.S. GDP in 2025—is economically significant and historically alarming. Fundamentally, it points to a broader macro-financial stability and policy credibility.

Deficit spending1 in the United States, which necessitates additional Treasury issuance over time, held steady near 2-4% of GDP for most periods between 1975 and the 2008 financial crisis. Notably, efforts in 1993 via higher taxes and in 1997 by way of bipartisan balanced budget legislation contributed to budget surpluses for a brief time. However, the long run pattern of deficit spending built up debt levels over the years, which jumped after the Great Financial Crisis (GFC) of 2008, and again post-Covid, as U.S. pandemic-related fiscal stimulus spending in the U.S. far exceeded tax revenues. Deficits are in the spotlight once again as budget watchdogs forecast deficit spending as a percentage of GDP will grow. “Current deficit spending of 7% of GDP already represents higher levels than any period in U.S. history besides post-GFC responses and the post-Covid period,” according to Merz. (Source: U.S. Treasuries: Balancing strong income and diversification opportunities with fiscal risks / US Bank)

Underlying everything are issues like

- unfunded entitlements

- rising interest payments on debt

- unsustainable defense and welfare outlays

So, a deficit as high as 7% of the GDP means that as we stand - government expenditures far exceed revenues, not merely due to emergency spending (like during COVID or the Global Financial Crisis), but also potentially due to persistent structural issues.

Clearly, the government is willing to borrow heavily even without immediate economic need. Long-term sustainability?

We are obviously looking for increasing and higher interest rates.

The thing is - investors and even other governments may begin to question the U.S. government’s ability or willingness to repay. This can destabilize the Treasury market and force emergency corrective actions (rate hikes, spending cuts), risking recession.

On May 16, 2025, Moody's Investors Service downgraded the US government's credit rating to Aa1 from Aaa, making it the last of the three major credit rating agencies to strip the U.S. of its AAA rating. This downgrade followed similar actions by S&P Global Ratings in 2011 and Fitch Ratings in 2023.

The primary reasons cited for the downgrade were rising government debt and interest payments, which Moody's noted were significantly higher than similarly rated sovereigns.

Last year , 2024, the interest payments in the US exceeded the defense spending for the first time.

Federal spending on interest payments is forecast to hit $870 billion this year — exceeding the $822 billion that the nation will spend on defense in 2024, according to a recent analysis by the Congressional Budget Office. This year's outlay for interest payments represents a 32% increase from last year's $659 billion in interest expense. To be sure, higher interest rates aren't the only factor raising the cost of servicing the country's debt. Over the last decade, the U.S. has almost doubled its outstanding debt, which surged to $33 trillion last year from $17 trillion in 2014, according to Treasury data. (Source: U.S. interest payments on its debt are set to exceed defense spending. Should we be worried? / CBS News)

Why is this important?

In February 2025, Nial Ferguson wrote how debt can impact the longevity of the major powers.

Ferguson's argument that great powers fall when their interest payments exceed their defense spending is now known as "Ferguson's Law."

Are there financial determinants of great-power decline and fall? This paper proposes “Ferguson’s Law,” which states that any great power that spends more on debt servicing than on defense risks ceasing to be a great power. The paper identifies the “Ferguson limit,” or the point at which interest payments exceed defense spending, as the tipping point after which the centripetal forces of the aggregate debt burden tend to pull apart the geopolitical grip of a great power. This is because the debt burden draws scarce resources towards itself, reducing the amount available for national security, and leaving the power increasingly vulnerable to military challenge. Using historical case studies that are analogous to the situation of the modern United States as the dominant global power, the paper shows that it is very rare but not unprecedented for a great power to return to the right side of the Ferguson limit. The paper is timely, as the United States began violating Ferguson’s Law for the first time in nearly a century in 2024. (Source: Ferguson’s Law: Debt Service, Military Spending, and the Fiscal Limits of Power / Hoover Institution)

So, given the historical learning, the United States may be in trouble as an empire. The obvious question is can it survive as a country if its no longer an empire? Something we have looked into recently.

Throwing out the International Students

The Trump administration wants to stop Harvard University from enrolling any international students. Just for context, 27% of Harvard University's total enrollment is of the foreign students. There are approximately 6,793 international students enrolled at Harvard for the 2024-2025 academic year. Just as in other US universities, the top 5 source countries are China, Canada, India, South Korea, and the United Kingdom.

The Trump administration on Thursday said it would halt Harvard University’s ability to enroll international students, taking aim at a crucial funding source for the nation’s oldest and wealthiest college in a major escalation of the administration’s efforts to pressure the elite school to fall in line with the president’s agenda. The administration notified Harvard about the decision — which could affect about a quarter of the school’s student body — after a back-and-forth in recent weeks over the legality of a sprawling records request as part of the Department of Homeland Security’s investigation, according to three people with knowledge of the negotiations. The people spoke on the condition of anonymity because they were not authorized to discuss the matter publicly. (Source: Trump Administration Says It Is Halting Harvard’s Ability to Enroll International Students / New York Times)

For now, the judiciary has halted the order.

A federal judge on Thursday extended an order blocking the Trump administration’s attempt to bar Harvard University from enrolling foreign students. U.S. District Judge Allison Burroughs extended the block she imposed last week with a temporary restraining order, which allows the Ivy League school to continue enrolling international students as a lawsuit proceeds. Harvard sued the federal government on Friday after Department of Homeland Security Secretary Kristi Noem revoked its ability to host foreign students at its campus in Cambridge, Massachusetts. (Source: AP News)

The unfolding legal contest around the proposed ban on foreign students echoes a familiar judicial rhythm in the United States, where executive overreach often collides with constitutional guardrails.

Preliminary court rulings already suggest that this latest maneuver may struggle to survive sustained legal scrutiny. Historical precedent offers a compelling clue: during the summer of 2020, the Trump administration’s attempt to expel foreign students enrolled in fully online programs met fierce resistance.

When Harvard and MIT challenged the policy, it was swiftly withdrawn, exposing the fragility of such unilateral immigration directives under judicial examination.

This current episode appears to be walking a similar trajectory. While the political optics may serve a momentary nationalist impulse, the legal infrastructure underpinning American higher education—and the rights of international scholars—remains more resilient.

Litigation will likely delay the implementation of the ban, if not nullify it entirely. The American judiciary, particularly in matters involving immigration and education, has historically leaned toward preserving institutional integrity and due process.

More importantly, Trump's pronouncements and actions are two veery different things. His statements and initial actions are geared more for disruption than actual policy change. The policy ostensibly reverts back to what it always was, but after it has done enough damage.

You see, the mere announcement of the Harvard foreign-student ban – and threats to extend it broadly – have sent shockwaves internationally.

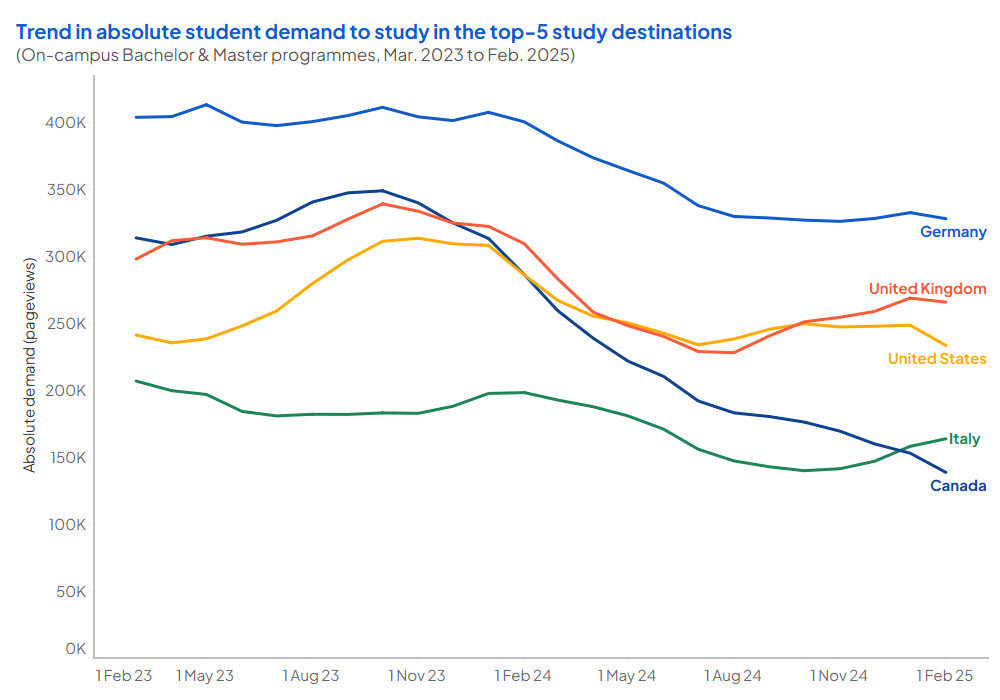

Students sitting outside of US are looking to the route to study in the US with significant trepidation.

A study reporting a 38% drop in international interest in U.S. master’s and PhD programs during the first quarter of 2025.

For some background, in early 2023, the U.S. rose to become the second-most sought-after study destination due to restrictive visa policies in the UK and Canada. However, demand stagnated and slightly declined by 2025, especially around the U.S. presidential elections. In contrast, student interest in the UK rebounded, driven by perceptions of greater political stability, more favorable visa policies, and renewed government support for international education. The British Council recently noted this shift, attributing the UK's rising appeal to its academic parity with the U.S. and its proactive efforts to attract and retain international students.

This restrictive U.S. stance is likely to redistribute significantly global student flows. Many of the approximately 1 million students who might have chosen the U.S. will turn to Canada, the UK, Australia, and Europe, with a portion staying in or attending rising Asian institutions. Over time, the U.S. could lose its position as the “reigning champion” of international education, a title it has already been slipping on in recent years.

Sudden removal of and decline in the international student population will start impacting the universities and their campuses wil start impacting more widely.

According to projections by the National Foundation for American Policy (NFAP), a sweeping ban on international students could precipitate a marked contraction in U.S. higher education over the coming decade. Specifically, undergraduate enrollment is forecasted to decline by 2%, while graduate programs could see an 11% collapse in admissions. These figures are not mere abstractions—they portend institutional shrinkage, with certain academic programs forced to scale back or shutter entirely due to enrollment shortfalls.

The consequences would not be confined to international students alone. American students, often misled into believing such policies serve their interests, would confront a diminished academic landscape: fewer course offerings, particularly in specialized or research-intensive disciplines, where international participation has long been a cornerstone. Larger student-to-faculty ratios would strain instruction, and faculty retention could suffer amid declining revenues. The result? A measurable decline in pedagogical quality and academic breadth.

According to projections by the National Foundation for American Policy (NFAP), a sweeping ban on international students could precipitate a marked contraction in U.S. higher education over the coming decade. Specifically, undergraduate enrollment is forecasted to decline by 2%, while graduate programs could see an 11% collapse in admissions.

It would be a folly to ignore these figures as mere mere abstractions.

The fact is that they point to institutional shrinkage. Why, because certain academic programs are forced to scale back or shutter entirely due to enrollment shortfalls.

American students will have to deal with a diminished academic landscape: -

Larger student-to-faculty ratios would strain instruction, and faculty retention could suffer amid declining revenues. The result? A measurable decline in pedagogical quality and academic breadth.

There is another area which will be impacted - innovation.

Roughly one-quarter of U.S. billion-dollar startup companies (unicorns) were founded or co-founded by former international students.

In the US today, there are nearly 180 billion-dollar US companies that were founded or co-founded by a former international student. Former international students make up nearly 25% of billion-dollar startup companies in the US, creating on average, 800 jobs per startup. (Source: Interstride)

Also, remember that with the startups that the international students create, they set up a culture for success in the US.

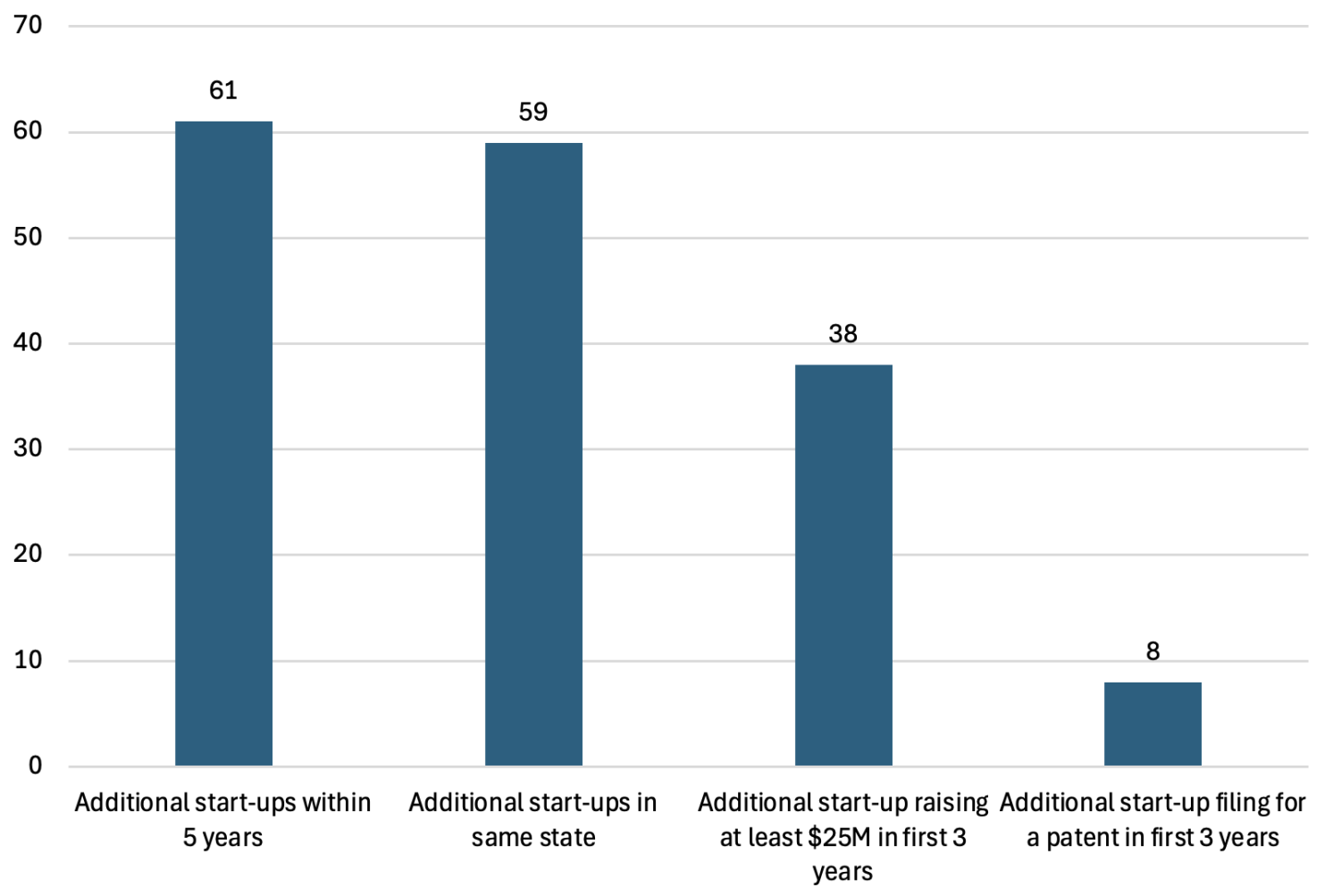

Our estimates imply that an additional 10,000 international master’s graduates would generate 61 additional startups by people in their master’s programmes, recorded in Crunchbase within five years of that cohort’s graduation (see Figure 1). This is significantly more than the simple average startup rate of master’s students in our sample and captures a combination of direct effect and spillover on classmates in creating startups. The result is in line with studies showing that immigrants in general, and foreign students in particular, are overrepresented among entrepreneurs in the US (Azoulay et al. 2022, Anderson 2022, Kerr 2013, Kerr and Kerr 2020). Crunchbase records tend to over-represent the more successful startups, as 98% of our sample survive at least three years. Hence, this effect is even more significant than simply adding startups, many of which do not succeed. Additionally, the increase in international students not only increased startup rates, but specifically increased the rate for highly valuable and innovative startups. Figure 1 shows that a significant boost was given to startups raising $25 million or more in capital within the first three years of creation (38 additional firms per 10,000 foreign master’s graduates) and to startups that file at least one patent in the first three years (eight additional firms per 10,000 foreign graduates). (Source: International graduate students and US startup creation / Centre for Economic Policy Research (CEPR))

Here is the graph illustrating the information shared above.

This is besides the $44 billion that international students spend within the US.

The United States is currently home to more than 1.1 million international students, more than half of whom come from India and China. During the 2023-2024 school year, international students are estimated to have poured almost $44 billion into the U.S. economy, according to NAFSA, a nonprofit association of international educators. (Source: Foreign Policy)

The losses in the short term, therefore, may not be that much, but in the long term, they will be huge.

The fear and the uncertainty will strip the US of its ability to attract the best of students and consequently the loss of future startups, which may come up outside.

Already, there are signs of high-end technocrats moving out of the US to start their own ventures in critical area of semi-conductors.

About a dozen executives from semiconductor and chip design companies such as Intel, AMD and Texas Instruments have quit to establish AI chip startups in India to tap into the multibillion-dollar industry. Four from Texas Instruments have started C2i Semiconductors, which is developing products to reduce energy consumption by semiconductors. They have raised $4 million from Yali Capital and Intel CEO Lip Bu-Tan, according to Tracxn. Bodhi Computing, which was acquired by Krutrim, was started by two Intel veterans, Sambit Sahu and Raghuraman Barathalwar. They are currently heading Krutrim’s semiconductor initiatives, which ET had reported earlier. Four former Intel and AMD executives have set up Agrani Labs and are developing indigenous AI chips in Bengaluru. They are in talks to raise $8 million from Peak XV Partners, according to people familiar with the development. Most of these executives have spent 15-20 years in the semiconductor industry. (Source: Intel, AMD former executives throw the hat into AI semiconductor ring / Economic Times)

So the question to ask is - was this targeting for foreign students really necessary?

Who's next - Even Naturalized Citizens are on the line

That is not an outlandish question.

Tucked among the priorities listed in his Day 1 executive orders was a one-line reference to enforcing a section of immigration law under which the government can revoke an immigrant's U.S. citizenship if it was "unlawfully procured." The directive is listed in the order called "Protecting the United States from Foreign Terrorists and Other National Security and Public Safety Threats." It's an indication that denaturalization will be part of his crackdown, said Amanda Frost, a University of Virginia law professor and immigration attorney. "We saw what happened last time," Frost said. "A lot of resources were put into denaturalization." Trump's new directive got little attention amid the flurry of eye-catching orders to launch the president's promised "mass deportation." In his first week, the president declared a national border emergency; deployed 1,500 troops to the border, including a combat force; and deputized thousands more federal law enforcement officers to arrest immigrants, among other moves. But this quiet, back-office directive has immigrant advocates worried because of the wide net his administration cast the last time. (Source: Trump revives push to denaturalize US citizens / USA Today)

This anxiety is not unfounded.

Remember that under Attorney General Jeff Sessions, the Trump administration had reviewed 700,000 naturalization files, seeking to bring 1,600 denaturalization cases to court as part of its broader "zero tolerance" immigration policy — a campaign that had become infamous for family separations at the southern border.

The implications are chilling: even citizenship, once considered the ultimate legal safeguard, is no longer immune to political targeting.

The renewed executive actions now threaten to revive that same climate of suspicion, one where legality is insufficient armor, and belonging feels conditional.

If these outlandish actions were the only ones by the administration, one could try to make sense of them. But things have gotten worse.

Specifically, how Trump administration has made its choices clear within the Indian subcontinent region. It has chosen to go with a terror state and leave India to deal with the mess that comes along with that.

Trump and America's love for a Terror State

Creating an alternative universe set of arguments, first the IMF and now the World Bank are busy sending funds to Pakistan (which is controlled by its military and corrupt politicians who divert these to terror infrastructure and their own accounts), while Trump administration is setting Pakistan up as the crypto capital of South Asia.

Let's start with the last one first.

In April 2025, Pakistan signed a cryptocurrency agreement with World Liberty Financial (WLF), a firm co-founded by Trump allies and majority-owned (60%) by the Trump family.

The deal, facilitated by the newly formed Pakistan Crypto Council, aimed to establish a strategic Bitcoin reserve and promote blockchain initiatives. The Pakistani Crypto chief was in Vegas recently selling Pakistan's great "achievements" in the Bitcoin conference.

If you want to understand what was done, please check this video from the X handle @speaknsee. Here is the link.

Internationally, the agreement raised concerns about potential conflicts of interest, especially as President Trump concurrently claimed credit for mediating peace between India and Pakistan.

A month before President Trump’s inauguration, Middle East envoy Steve Witkoff flew to the United Arab Emirates with two goals: discussing regional issues with the Abu Dhabi royal known as the “spy sheikh,” and attending a cryptocurrency conference. Less than five months later, Witkoff’s son, co-founder of the crypto venture World Liberty Financial, took the stage at a conference in Dubai to announce the company had struck a deal for the sheikh’s company to buy $2 billion of their new cryptocurrency. The expected tens of millions of dollars in annual profits would be split between the Witkoffs and their co-founders—and the Trump family, which holds a 60% stake in the company. (Source: Wall Street Journal)

The U.S. Senate initiated an inquiry into the deal, scrutinizing the intertwining of diplomatic efforts and private business interests.

India, perceiving the U.S.-Pakistan crypto collaboration as a geopolitical shift, expressed distrust towards the U.S., potentially impacting regional alliances and economic forecasts.

The Crypto Deal with Pakistan

If one looks at the details of Pakistan Crypto Council and WLF's deal, it is quite plausible to argue that the Pakistan Crypto Council (PCC) and the World Liberty Financial (WLF) deal—especially with the Trump-linked revival of engagement—could be part of a broader scheme that involves:

Collateralizing Pakistan's National Assets via Crypto Structures

Pakistan is in economic free fall. It lacks liquid assets but owns high-value strategic infrastructure: Gwadar Port, airports, railways, copper/gold mines, and CPEC-linked zones. In the absence of IMF-style oversight, tokenizing these state assets as "collateral" for stablecoins or sovereign crypto-debt can serve as a workaround to raise opaque funds:

- Crypto tokens pegged to state infrastructure could be issued with little transparency or parliamentary oversight.

- These assets may be de facto pledged to WLF and its associates in exchange for dollar-denominated crypto liquidity, bypassing global regulatory scrutiny.

- This turns critical Pakistani national infrastructure into blockchain-registered hostages—open to seizure or exploitation by shadow financiers.

This is essentially a digital pawn scheme: Pakistan offers up its crown jewels for quick access to opaque funds, with long-term sovereignty losses.

Using Crypto's Opacity to Channel Terror Financing

Crypto’s pseudo-anonymity and ease of cross-border transfers make it an ideal vehicle for:

- Funding proxy jihadist groups like Lashkar-e-Taiba, Haqqani Network, or TTP without involving traditional banking channels.

- Paying mercenaries, acquiring arms, or laundering funds through crypto mixers and offshore wallets.

- Avoiding FATF and SWIFT scrutiny, which Pakistan’s banks face under terrorism-financing suspicions.

The Trump-linked WLF’s entry, if aligned with crypto-based bond or investment instruments, could become a shield for elite asset siphoning and clandestine operations, especially under geopolitical cover stories like “digitizing emerging markets.”

So, the PCC-WLF construct could well be a cover for weaponizing Pakistani state assets and crypto liquidity to:

- Bail out the elite through debt-for-asset swaps,

- Fund radical groups under radar,

- And bypass IMF/World Bank/UN scrutiny.

This represents a geopolitical fusion of terror financing, crypto opacity, and elite asset monetization, with the Trump administration’s involvement giving it legitimacy and cover.

The Financial Institutions as Terror Guarantors

Just a few days after the deadly terror attack against India, backed by Pakistan, the IMF awarded it with a bailout of $2.1 billion.

The International Monetary Fund (IMF) is facing sharp criticism for approving a $1 billion disbursement to Pakistan just days after a deadly terrorist attack in Kashmir’s Pahalgam and amid escalating hostilities between India and Pakistan. The disbursement, approved on Friday under the Extended Fund Facility (EFF), raises total payouts under the programme to $2.1 billion. Additionally, the IMF cleared $1.4 billion under the Resilience and Sustainability Facility (RSF), ostensibly aimed at helping Pakistan tackle climate-related vulnerabilities. (Source: India Today)

The Indian administration called it out the way it is.

All this when Pakistan was placed on the FATF's grey list in 2018 due to shortcomings in its anti-money laundering/counter-terrorism financing (AML/CFT) framework. This meant Pakistan was under heightened scrutiny and subject to increased monitoring by the FATF.

And now, the World Bank has also jumped into the ring to help the poor terror backing Pakistan with a proposed $40 billion investment.

Marketed as support for infrastructure, education, and climate resilience, it risks becoming a booster shot for Pakistan’s deeply embedded terrorism infrastructure.

With a long history of diverting international aid toward extremist networks and proxy warfare, Pakistan’s military-intelligence complex, notably the ISI, has repeatedly channeled global funds into sustaining groups like Lashkar-e-Taiba, Jaish-e-Mohammed, and the Taliban.

Under the guise of “development,” the military-run economy benefits from inflated contracts, land grabs, and resource control—fuelling jihadi narratives and recruitment.

With the new funds, the Army will push into the conflict-prone areas like Balochistan or Khyber Pakhtunkhwa to further massacre the local populations.

This practiced ignorance and excitedly hopeful reaction of the Western elites and the media in "helping Pakistan" is not new.

Dr. Robert E. Looney, Professor of National Security Affairs and Associate Chairman of Instruction at the Department of National Security Affairs, Naval Postgraduate School, Monterey, California, sounded so cute when he asked these questions in his 2004 article titled "Failed Economic Take-Offs and Terrorism in Pakistan: Conceptualizing a Proper Role for U.S. Assistance" for Asian Survey.

Terrorism was and even now is treated by the West as a variable that competes with economic indicators. It is not!

In Pakistan's case, it's a choice: a geopolitical and a religious/ideological choice to hit India.

The almost bankrupt economy is a consequence. As are the many massacres that the group of war criminals masquerading as the Army has been unleashing over the many decades.

So let's not kid ourselves about the recent altruistic actions by the US and the institutions.

Where are we headed?

The convergence of troubling economic indicators has reignited anxieties—not just of a cyclical downturn, but of a global recession, a prolonged depression, or the chilling prospect of systemic collapse. While current growth forecasts by major institutions appear modestly stable, they obscure the tectonic instability underneath.

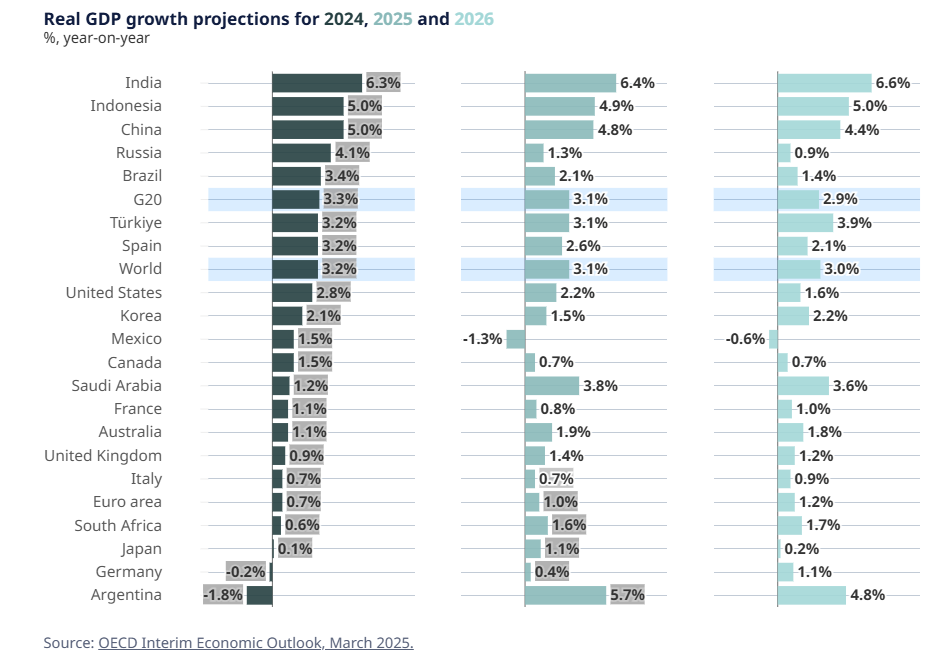

The International Monetary Fund (IMF) projects global GDP growth to hover between 2.8% and 3.3% through 2025–2026. The OECD echoes this caution, forecasting 3.1% in 2025, falling to 3.0% in 2026. Morgan Stanley anticipates 2.9% and 2.8%, respectively. On the surface, these figures represent modest deceleration. But in reality, they signal a global economy losing momentum—slipping below historical thresholds of resilience, and increasingly vulnerable to even mild disruptions.

OECD shares these predictions for the growth rates.

Not just the OECD, but a whole host of think-tanks are concerned about the economies around the world, but do not equate it to the 1930 style depression.

While a 1930s-style global depression may actually be unlikely because of safety nets and more responsive policy mechanisms.

However, this may be “lost decade” in terms of the economy.

For heavily indebted nations or those resistant to structural reforms, the future may be marked by stagnant growth, persistent fiscal pressure from rising debt servicing, and chronic underinvestment in critical sectors.

Such conditions can entrench economic malaise, erode competitiveness, and amplify social unrest. The threat is not collapse, but a prolonged erosion of dynamism—where economies drift without momentum, and recovery remains elusive. In this scenario, resilience is not guaranteed by policy tools alone, but by the political will to undertake deep, often painful, transformation.

Now add fire to this slow burn.

The world’s geopolitical architecture is not only shifting—it is fracturing. The once-ironclad Transatlantic alliance is showing strain. NATO is no longer immune to internal rifts. U.S.–European relations are tested by divergent priorities, energy crises, and growing American unpredictability.

Meanwhile, the U.S.–China cold conflict continues to metastasize into every sphere—economic, technological, and military. Russia, far from isolated, is now firmly aligned with Beijing, and emboldened by a fragmented West.

And perhaps most consequential of all: India, once courted as a strategic counterbalance, now views the United States with deepening distrust. The Biden and Trump administrations’ overtures to Pakistan, including tacit support and strategic deals, have shattered whatever fragile confidence remained in the Indo-U.S. relationship. For New Delhi, the betrayal is not just diplomatic—it’s civilizational.

What does this mean for the global economy?

It means decoupling, derisking, and fragmentation—the antitheses of global growth.

It means supply chains becoming weaponized, capital flows turning political, and trade policies driven by ideology over efficiency.

It means the disintegration of trust that once underpinned financial and commercial systems.

With no trusted center of gravity, markets begin to untether.

Thus, even if the numbers do not yet scream collapse, the subtext is loud: a slowing world economy hemmed in by uncertainty, stripped of unity, and encircled by rival blocs. Predictive models, rooted in peacetime assumptions, now struggle to capture the volatility of a post-American, post-unipolar, mistrust-driven world.